Here is an important retirement planning tip — most members can create their own pension estimate in minutes using Retirement Online. Your estimate will be based on the most up-to-date account information we have on file for you. You can enter different retirement dates to see how those choices would affect your benefit. When you’re done, you can print your pension estimate or save it for future reference.

Remember, the pension amounts you’ll see are just an estimate; it is not a guarantee of what you’ll receive when you retire.

Most Tier 2 through 6 members (more than 90 percent of all NYSLRS members) can use the Retirement Online pension calculator. However, some members may not be able to because of their circumstances — for example, members who recently transferred to NYSLRS, some PFRS members, or Tier 6 members with between five and ten years of service. The system will notify you if your estimate cannot be completed using the Retirement Online pension calculator. Please contact us to request a pension estimate if you receive this notification.

Planning on taking out a NYSLRS loan? Applying through Retirement Online is fast and convenient.

Eligibility for a NYSLRS loan is based on your tier. Generally, you’ll need to be on the payroll of a participating employer, have at least one year of service and have sufficient contributions in your account. (Note: Retirees are not eligible for NYSLRS loans.)

Retirement Online is the Fastest Way to Apply

When you use Retirement Online, NYSLRS receives your application immediately and can process your loan more quickly. It’s also an easy way to check the amount you are eligible to borrow, your balance on any outstanding loans, and more.

In the ‘I want to…’ section, click the “Apply for a Loan” button.

Follow the prompts.

As you work your way through the online application, you’ll see:

How much you are eligible to borrow;

The minimum repayment amount;

The expected payoff date; and

How much you can borrow without tax implications.

If you apply for a loan and you already have an existing loan (or loans), you’ll choose one of two options:

Multiple loans: With multiple loans, you are taking a new loan, and each of your outstanding loans has a separate five-year due date and minimum payment. The minimum payments for each of your loans are added together for one total minimum payment. This combined minimum payment amount is higher than the minimum would be if you choose a refinanced loan, but with multiple loans, as each loan is paid off, your total minimum payment goes down.

Refinance your existing loan: Refinancing your loan adds your new loan amount to your existing balance and consolidates the entire amount as one loan instead of taking separate loans. Minimum payment amounts for refinanced loans are lower than the minimum for multiple loans because when you refinance, we combine your existing loan balance with your new loan and spread out the repayment over a new five-year term. However, this increases the portion of your loan that may be considered a taxable distribution, and federal withholding can significantly reduce the loan amount that you receive.

There is a service charge of $45 that will be deducted from your loan check when it is issued. The current interest rate is 5 percent. The interest rate will remain fixed for the term of your loan.

If your case status says “Closed” before close of business on Wednesday, your check will be in the mail that Friday.

You will also receive a confirmation letter when your loan case has been completed. You can find it in your Retirement Online account under “View Documents.”

Repaying Your NYSLRS Loan

Loan payments are deducted from your paycheck. If you choose to repay the minimum amount, your payroll deduction may be increased periodically to ensure your loan will be repaid within the required five-year repayment term. You can increase your payroll deduction amount, make additional payments or pay your loan in full at any time with no prepayment penalties. Retirement Online is the easiest way to manage your loan payments. Sign in to your account and select “Manage my Loans.”

Retiring With an Outstanding NYSLRS Loan

If you retire with an outstanding loan, your pension will be reduced. You will also need to report at least a portion of the loan balance as ordinary income (subject to federal income tax) to the IRS. If you retire before age 59½, the IRS may charge an additional 10 percent penalty. If you are nearing retirement, be sure to check your loan balance. If you are not on track to repay your loan before you retire, you can increase your loan payments, make additional lump sum payments or both in Retirement Online.

Note: Employees’ Retirement System (ERS) members may repay their loan after retiring, but they must pay the full amount (that is, the amount that was due on their retirement date) in a single lump-sum payment. Once you do, your pension benefit will increase from that point on, but it will not be adjusted retroactively back to your date of retirement.

Visit Our Website for More Information

For more information about NYSLRS loans, including what happens if you go off payroll or default on your loan, visit our Loans page. Need help with Retirement Online? See our Tools and Tips blog post.

NYSLRS retirement plans provide death benefits for beneficiaries of eligible members who die before retiring. If you are retired, your beneficiaries may be entitled to a post-retirement death benefit.

It’s important to name beneficiaries and review them periodically. Life circumstances sometimes change, and the beneficiary you named before might not be the one you would choose today. For example, if you just married, you may want to update your NYSLRS account information to name your new spouse as your beneficiary.

2 Types of Beneficiaries

Your primary beneficiary will receive your death benefit. You can list more than one primary beneficiary. If you do, they will share the benefit equally. Or you can choose different percentages for each beneficiary to total 100 percent. (Example: John Doe, 50 percent; Jane Doe, 25 percent; and Mary Doe, 25 percent.)

A contingent beneficiary will only receive a benefit if all your primary beneficiaries die before you do. If you list multiple contingent beneficiaries, they will share the benefit equally unless you choose different percentages.

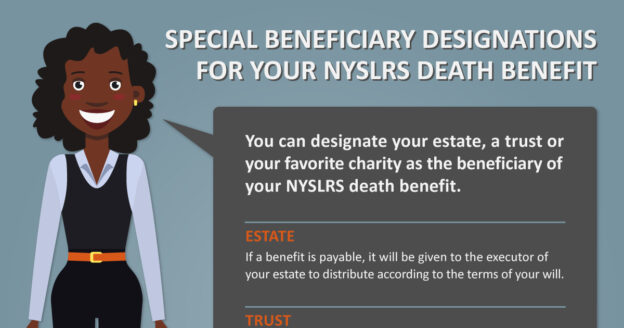

Special Beneficiary Designations

Your beneficiary doesn’t have to be a person. You can name a charity, a trust or your estate as your beneficiary.

Estate. When you die, your estate is the money and property you owned. Your death benefit will be given to the executor of your estate to be distributed according to the terms of your will. You can name your estate as the primary or contingent beneficiary of your death benefit. If you name your estate as the primary beneficiary, do not name a contingent beneficiary.

Trust. You can name a trust as a primary or contingent beneficiary if you have a trust agreement or provided for a trust in your will. The trust itself would be your beneficiary, not the individuals for whom you established the trust. (Speak with your attorney if you’re thinking about making your trust a beneficiary.)

Entity. You can also name any charitable, civic, religious, educational or health-related organization as a beneficiary.

Minor children. If your beneficiary is under the age of 18 at the time of your death, your benefit will be paid to the child’s court-appointed guardian. You may instead choose a custodian to receive the benefit on the child’s behalf under the Uniform Transfers to Minors Act (UTMA). Custodians can be designated in Retirement Online or you can contact us for more information and the appropriate form before making this type of designation.

Keep Your Beneficiaries Up to Date

You can change your beneficiaries at any time. In addition to adding or removing them to reflect your current wishes, you should review the contact information for your named beneficiaries so we can find them when needed.

The fastest way to view or update your beneficiaries is in Retirement Online.

Member Annual Statements are distributed to NYSLRS members each spring. Don’t wait for a mailed copy — get your Statement online instead! You can update your delivery preference in Retirement Online to receive an email when your Statement is available.

From your Account Homepage, click “update” next to ‘Member Annual Statement by.’

Choose “Email” from the dropdown.

Check and Update Your Contact Information

Retirement Online is the fastest way to check your contact information and update it if needed. If you don’t already have an email address on file, please provide it so that we can contact you quickly if we need to notify you about important information such as a change to your benefits. Use a personal email address you will have access to before and after you retire, rather than a work email address. You should also make sure your mailing address and phone number are current.

To update your contact information, click “update” next to your email address, mailing address or phone number to make corrections.

Use Retirement Online to Stay Informed

Your annual Statement is a snapshot of your NYSLRS account as of March 31. For the most up-to-date information year-round, sign in to your Retirement Online account.

In Retirement Online, you can view your date of membership, tier, retirement plan, estimated total service credit and more. Check out what else members can do in Retirement Online.

When it comes to managing your NYSLRS account, Retirement Online is the fastest way to do it. Skip printing forms, having them notarized and sending them through the mail — when you submit your requests online, NYSLRS has them immediately and your changes will be completed more quickly. It’s convenient, and it’s secure.

Here’s a look at some of the things NYSLRS members (not yet retired) can do online.

View Your Account Information

Sign in to Retirement Online for easy access to key information to help you plan for retirement. On your Account Homepage, you can find your date of membership, tier, retirement plan (which you can use to find your retirement plan publication), estimated total service credit and more.

Change Your Delivery Preference to Email and Help Us ‘Go Green’

Save time and reduce paper waste — help us ‘go green’ by choosing the paperless option. When you choose to receive information from NYSLRS electronically, we will send you an email when important documents and letters are ready to view in Retirement Online.

From your Account Homepage, click the “update” link next to ‘Contact by’ or ‘Member Annual Statement by.’

Choose “Email” from the dropdown menu.

If you choose “Email” as your delivery preference, you will not receive a printed copy in the mail.

Update Your Contact Information

It’s important that we have your current contact information so you receive the news, letters and statements that we send you. You can update your email address, mailing address and phone number in the ‘My Profile Information’ section of your Account Homepage. Just click “update” next to the item you’d like to change. Use a personal email address that you will have access to before and after you retire, rather than a work email address.

View and Update Your Beneficiary

NYSLRS retirement plans provide death benefits for beneficiaries of eligible members who die before retiring. It’s a good idea to review your beneficiaries from time to time to make sure your choices reflect your current wishes. Retirement Online is the fastest way to add or remove beneficiaries or update their contact information. Click the “View and Update My Beneficiaries” button to get started.

Estimate Your Pension

How much will your pension be? It’s an important question as you’re planning for retirement. In just a few steps, most members can estimate their retirement benefit based on up-to-date account information, then save or print the estimate. Entering different dates and comparing the results can help you choose the retirement date that’s right for you. From your Account Homepage, click the “Estimate my Pension Benefit” button.

Apply for a Loan and Manage Loan Payments

It’s easy to apply for a loan in Retirement Online. If you are eligible to take a loan against your retirement contributions, you can see how much you can borrow, your repayment options and whether your loan will be taxable — all before you apply. Click the “Apply for a Loan” button to start an application.

If you have an existing loan, you can click the “Manage My Loans” button to adjust your payment amount or to make an additional one-time payment.

Request Credit for Previous Service

If you worked for a participating public employer before joining NYSLRS, or if you served in the U.S. Armed Forces, you may be able to purchase service credit for that time. Click the “Manage My Service Credit Purchases” button to request credit and upload any supporting documentation.

Purchase previous service credit as soon as possible. It’s cheaper and will make it easier to calculate your final monthly pension payment.

Get Your Member Annual Statement Faster

Your Member Annual Statement can help you understand your benefits. It’s a snapshot of your NYSLRS account based on the information we have on file for you as of March 31 each year, the close of our fiscal year. Statements will be available online in the spring, sooner than printed copies will be mailed — update your delivery preference to “Email” to get notified when it’s available online.

Generate a Mortgage Verification Letter

If you need to provide proof of your NYSLRS account information for a mortgage, you can get your own income verification letter online. From your Account Homepage, in the ‘I want to…’ section at the top right, click the “Generate Income Verification Letter” link. You can print a document that shows your contribution balance, and — if you have an outstanding loan — the date of your last loan, the current balance and the interest rate.

Apply for Retirement

When you are ready to retire, Retirement Online allows you to skip the hassle of mailing paper forms or visiting our office. You can apply for a service retirement benefit, choose your pension payment option, sign up for direct deposit and submit retirement-related paperwork online. A big advantage of applying online is that you don’t have to get anything notarized. Read our blog post about applying for retirement for more information and links to resources.

Other Online Transactions

If you previously were a member of another New York State public retirement system before joining NYSLRS, your service could be recredited and your date of membership and tier restored. You can click the “Reinstate a Previous Membership” button to get started.

If you leave public employment with less than ten years of service credit, you can use Retirement Online to withdraw your membership. However, this will terminate your membership with NYSLRS. If you have any questions, speak with a customer service representative before you submit your withdrawal application. You can message them using our secure contact form.

If you need help accessing Retirement Online, here’s some handy information to help you register, sign in, reset your password and more.

Registering for Retirement Online

For security reasons, when you sign up for an account, you will be asked to identify yourself, confirm your Social Security number and verify your identity. Then you’ll be asked to create your user ID and password. Read our Registering for Retirement Online guide for help with the registration process.

After you sign in for the first time, you’ll be asked to choose security questions and submit answers. Make sure you remember your responses — you’ll need to answer these questions again if you are ever locked out of your account or need to reset your password.

Keep Your Password Current

Be sure to sign in at least once a year and update your password so it doesn’t expire.

Forgotten User IDs or Passwords

You can retrieve your user ID or reset your password on your own.

To look up your user ID, go to the Retirement Online sign-in page. Click the “Forgot ID” link above the User ID field. From there, you can identify yourself and answer security questions to receive your user ID. Read our Forgot User ID guide for step-by-step information.

If you’ve forgotten your password, click the “Forgot Password” link above the Password field. You’ll identify yourself with your user ID and answer security questions to reset your password. Read our Forgot Password guide for step-by-step information.

Account Lock Out

When signing in to Retirement Online, you have a limited number of attempts to enter your user ID and password correctly. After that, the system will lock your account for security purposes. If this happens to you, don’t worry. Most users can unlock their own account and set a new password in just five steps.

Click “OK” on the pop-up message saying your account is locked.

Select how you want to receive your security code and click “Next.”

Enter the security code you received and click “Submit.”

Correctly answer secret questions that you created when you first registered.

Enter a new password and click “Reset Password.”

What Web Browser to Use

Retirement Online works best in Microsoft Edge and Google Chrome. If you’re having trouble signing in, clearing your browsing data may help. Read our Clear Your Cache guide for step-by-step information.

Retirement Online is generally available:

Monday, Wednesday and Friday from 7:00 am to 10:00 pm

Tuesday and Thursday from 7:00 am to 6:00 pm

Weekends from 6:00 am to 11:00 pm

Over time, we will expand our hours to better serve you. For more information and the latest hours of availability, please visit our Retirement Online Sign In page.

You can find more information and tips on our Retirement Online page. If you need help, contact our customer service representatives for assistance. You can call them at 866-805-0990. Press 2 and follow the prompts. The Call Center is open Monday through Friday, from 7:30 am to 5:00 pm.

More than 480,000 members and retirees have discovered that Retirement Online is the fastest way to do business with NYSLRS. It’s secure and convenient, and helps you avoid calling or mailing forms. It also gives you instant access to information about your benefits. And, your important documents will be available online, sooner than printed copies are mailed.

Retirees Can Do Even More in Retirement Online

The Fastest Way to Get Your 1099-R Tax Document

With Retirement Online, you can get the tax information you need faster. If you receive a taxable benefit from NYSLRS, your 1099-R is now available online. Sign in to view, save or print your tax form for 2023.

View Your Retiree Annual Statement Online

Your Retiree Annual Statement provides important information about your benefit amount, deductions and tax withholding. Beginning with your 2023 Statement, you can now access it in Retirement Online.

Make the Switch to Email and ‘Go Green’

Be the first to know when documents are available online — email delivery gives you access to your important documents sooner. It also helps the environment by reducing paper consumption. ‘Go green’ by choosing the paperless option.

It’s easy to make the switch. To receive an email when your 1099-R tax form and Retiree Annual Statement are available in Retirement Online next year:

From your Account Homepage, click the “update” link next to ‘1099-R Tax Form Delivery by’ or ‘Retiree Annual Statement by.’

Choose “Email” from the dropdown.

Be sure to check that the email address listed in your Retirement Online profile is current.

If you choose the email delivery preference, you will not receive a printed copy in the mail.

Don’t Forget These Timesaving Features

Change Your Federal Tax Withholding

No forms needed — Retirement Online is the fastest way to update your withholding. If you submit your changes by the middle of the month, they will generally be applied to that month’s payment.

Generate a Pension Verification Letter

There are organizations that may ask you for a letter verifying your pension income — maybe for housing or as part of an application for the Home Energy Assistance Program (HEAP). You can use Retirement Online to save or print your own letter any time you need one.

Manage Your Direct Deposit

Use Retirement Online to securely update your direct deposit bank account information. Whether you’ve switched banks or need to move your deposits to a different account, you can make those changes quickly with Retirement Online. Changes are generally applied within one to two payments, and more quickly than if you send in a paper form.

View Your Pension Pay Stubs

You can access pay stubs for your benefit payments by clicking the date of the payment you want to view. You can track year-to-date totals and any deductions for health insurance, union dues, tax withholding or disbursements under a domestic relations order, giving you greater insight into your benefits. NYSLRS will also send you a notice whenever the amount of your monthly payment changes.

Update Your Contact Information

Let us know if you move or your phone number or email address change. Update your contact information quickly in Retirement Online to make sure you continue to receive important news and information about your benefits.

You can even schedule an address change, so you’ll get NYSLRS mail at your seasonal home without interruption.

Manage Your Beneficiaries

Eligible retirees can change their beneficiary for their post-retirement death benefit or update contact information for an existing beneficiary.

Your Retiree Annual Statement is now available in Retirement Online! Retirees who opted to go paperless already received an email notifying them that their Statement is available in their Retirement Online account.

If you did not change your delivery preference to email, your Statement will be mailed by the end of February.

Get Your Statement Online Now

Whether you chose email delivery or not, you can access your Statement in your Retirement Online account now. To view, save or print your Statement:

From your Account Homepage, click the “View My Retiree Annual Statement” button.

Follow the prompts.

If you don’t have an account, you can find step-by-step instructions for registering in the Tools & Tips section of the Retirement Online page.

Inside Your Retiree Annual Statement

Your Statement has a new look this year, but it still contains the same information you receive every year about your benefit amount, deductions and tax withholding. Your Retiree Annual Statement includes:

Your NYSLRS ID. To protect your privacy, use this number instead of your Social Security number when conducting business with NYSLRS.

The total amount of your annual benefit. (This is your base benefit, before taxes, deductions and credits.)

Your total net benefit for the year. (This is your benefit after taxes, deductions and credits.)

Other deductions taken from your pension, such as payments to an alternate payee or union dues.

Health insurance premiums. (NYSLRS doesn’t administer health insurance benefits, but we deduct retiree premiums at the request of your former employer.)

Next Year Don’t Wait for the Mail

Going forward, your Statement will be available online in early February each year.

Update your delivery preference now to receive an email as soon as next year’s Retiree Annual Statement is available online:

From your Account Homepage, click the “update” link next to ‘Retiree Annual Statement by.’

Choose “Email” from the dropdown.

If you choose to receive your Statement by email, you will not receive a printed copy in the mail.

Use Retirement Online to Stay Informed

Your Statement is a snapshot of your NYSLRS account as of December 31, 2023. For the most up-to-date information year-round, sign in to Retirement Online. If you don’t already have an account, you can learn more or register today.

In Retirement Online, you can view pay stubs for your benefit payments. Check them if you have a question or to track year-to-date totals of your pension benefit as well as any deductions for health insurance, union dues, tax withholding or disbursements under a domestic relations order.

Your Statement is Not a Tax Document

While your Retiree Annual Statement does include information about your benefit payments and tax withholding, it is not a tax document. If your pension is taxable, you should have received a 1099-R tax form (either through your Retirement Online account or by mail, depending on your delivery preference) for filing your taxes.

Tax season is approaching, and with 1099-Rs available online, getting this key NYSLRS tax form is now faster and more convenient than ever.

Most NYSLRS pensions are subject to federal income tax (some disability benefits are not taxable). If you receive taxable income from NYSLRS, we provide a 1099-R tax form for filing your taxes. New this year, retirees who opted to go paperless received an email notifying them their 1099-R is available in their Retirement Online account. If you did not change your delivery preference to email, your 1099-R tax form will be mailed to you by January 31.

Understanding Your 1099-R

A 1099-R tax form is used to report the distribution of taxable retirement benefits. It shows:

The total benefit paid to you in a calendar year.

The taxable amount of your benefit.

The amount of taxes withheld from your benefit.

If you have questions about the information on the form, check our interactive 1099-R tutorial. It walks you through a sample 1099-R and offers a short explanation of each box on the form.

Get Your 1099-R Online Now

Whether you chose email delivery or not, you can access your 1099-R in your Retirement Online account now. To view, save or print your 1099-R:

Retirees, brush up on your Retirement System knowledge!

Get Your 1099-R Tax Form in Retirement Online Starting in 2024, your 1099-R tax form will be available in Retirement Online! Get yours faster and help us ‘go green’ — update your delivery preference now to receive an email when it’s ready, instead of waiting for it in the mail. (If you choose to receive your 1099-R by email, you will not receive a printed copy in the mail. Regardless of your delivery preference, you will be able to view and print your 1099-R by signing in to Retirement Online at the end of January.)

Change Your Federal Tax Withholding in Retirement Online Retirement Online is the fastest way to update your withholding. Changes submitted by the middle of the month will generally appear in that month’s payment. Most NYSLRS pensions are subject to federal income tax (some disability benefits are not taxable).

Not Taxed by New York State Your NYSLRS pension is not subject to New York State or local income taxes. Visit our Taxes and Your Pension page for more information. If you move to another state, your pension may be subject to that state’s income tax. If you’re thinking of moving to another state, check with that state’s tax department.

Get Your Retiree Annual Statement in Retirement Online Starting in 2024, you can use Retirement Online to view and print your annual statement. Help us go green and update your delivery preference to receive an email when it’s available, instead of waiting to receive it in the mail.

Manage Your Direct Deposit in Retirement Online Use Retirement Online to securely update your direct deposit bank account information. Whether you’ve switched banks or need to move your deposits to a different account, you can make those changes quickly with Retirement Online. Changes are generally applied within one to two payments. You can find out when your next pension payment is coming by checking our online pension payment calendar.

Prove Your Pension Income Using Retirement Online You may need proof of your retirement income for housing or as part of an application for the Home Energy Assistance Program (HEAP). With Retirement Online, you can print or save an income verification letter any time you need one.

Receiving Your Annual Cost of Living Increases Once you become eligible for a cost-of-living adjustment (COLA), you will receive a permanent increase to your pension amount every September. When your net benefit amount changes, NYSLRS will inform you.

View Your Pension Payment “Pay Stub” in Retirement Online Sign in to Retirement Online to access full pay stubs for your pension payments. Select the date of the payment you want to review to see a breakdown of your pension payment, including your most recent COLA amount as well as any deductions made for health insurance, union dues, tax withholding or disbursements under a domestic relations order.

You May Leave a Death Benefit Your survivors may be entitled to a death benefit after you die. Retirement Online makes it easy for eligible retirees to view their beneficiary selections, choose different beneficiaries or change contact information for an existing beneficiary. Anyone can report the death of a retiree by using our online death report form.

Best-Funded, Best-Managed The New York State Common Retirement Fund holds and invests the assets of NYSLRS on behalf of members, retirees and their beneficiaries and continues to be one of the best-funded and best-managed public pension funds in the nation. Comptroller Thomas P. DiNapoli is the administrative head of NYSLRS and trustee of the Common Retirement Fund.

Tax season is approaching, and with 1099-Rs available online, getting this key NYSLRS tax form is now faster and more convenient than ever.

Tax season is approaching, and with 1099-Rs available online, getting this key NYSLRS tax form is now faster and more convenient than ever.