The coronavirus (COVID-19) has disrupted our daily lives in ways large and small. As New York and the rest of the nation work on treatment and containment of this virus, many New Yorkers are concerned about what the future will bring.

The New York State and Local Retirement System (NYSLRS) wants to assure retirees and members who rely on the state pension fund for fiscal security that it is well positioned to weather the volatility in the financial markets. Your retirement benefits are secure and you will continue to receive your pension payments.

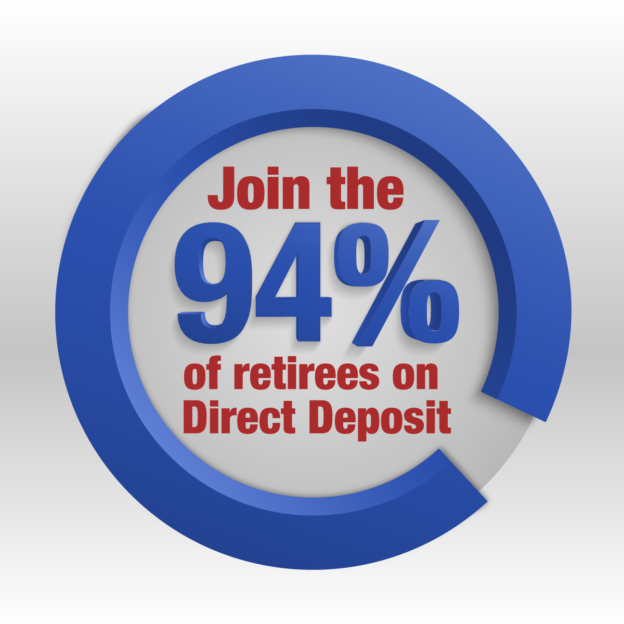

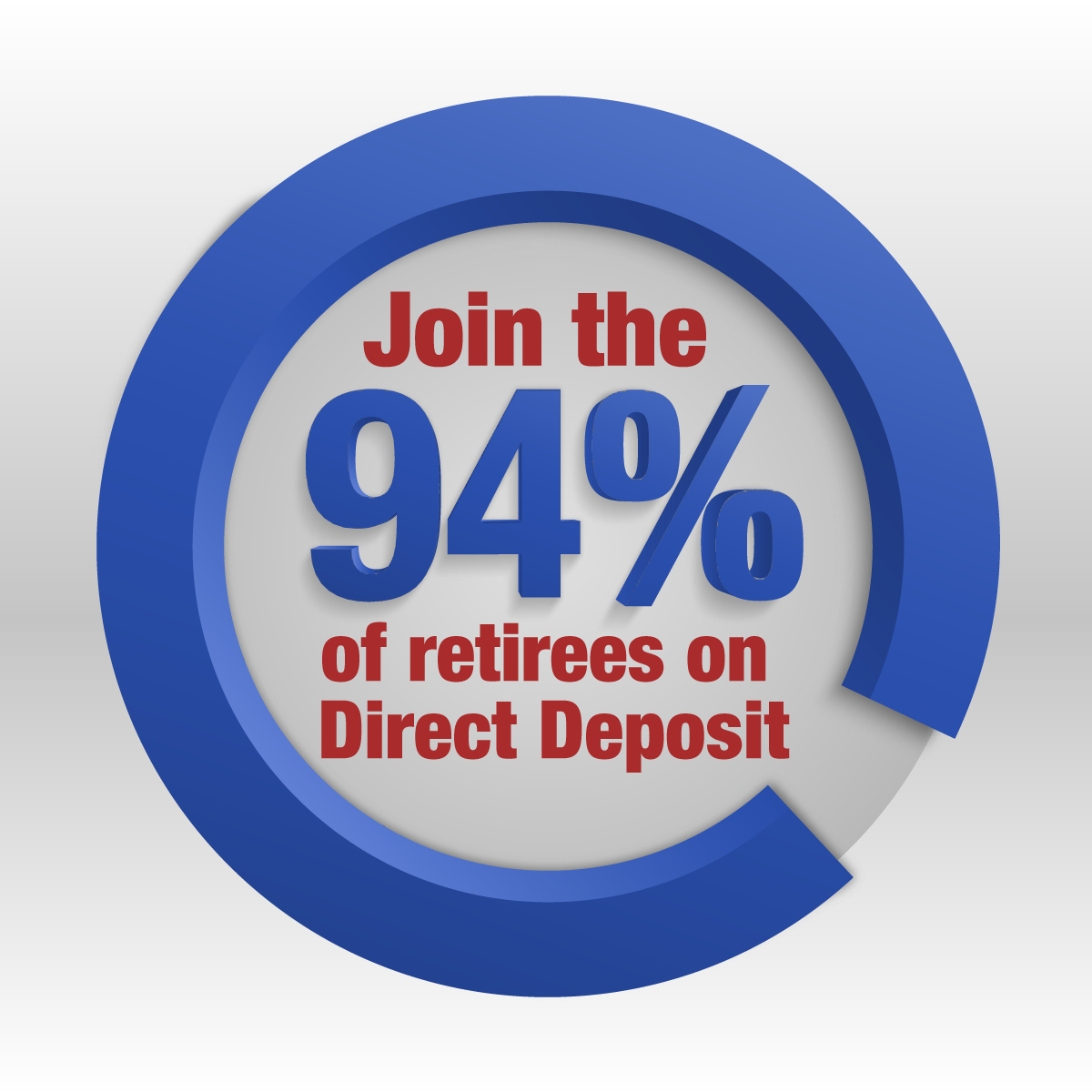

Retirees: Please Sign Up for Direct Deposit

As NYSLRS closely monitors the public health measures being taken to prevent the community transmission of the coronavirus, there are circumstances that could arise that impact the delivery of pension checks, particularly the ability of retirees to go to the bank to deposit them.

NYSLRS strongly urges retirees to consider signing up for direct deposit, instead of receiving a monthly pension by check via mail delivery. The vast majority of our retirees have their retirement and Social Security benefits deposited directly into their checking or savings account. Direct deposit is quick and safe. To enroll in direct deposit, complete the Electronic Funds Transfer Direct Deposit Enrollment Application (RS6370).

I was informed when I retired last year that it would take anywhere from 18 months to 22 months to calculate my accruals to determine my final monthly distribution amount. Is that still the case or was this process put on hold due to COVID 19?

During the COVID-19 emergency, NYSLRS’ essential staff continues to do Retirement System work. We are processing mail and applications, answering phone calls and responding to emails during this time.

For questions about current processing times, please email our customer service representatives using the secure email form on our website. Filling out the secure form allows them to safely contact you about your personal account information.

Did Governor Cuomo release a bill allowing an extension for retirees in the amount of money that can be made or money made between March 27th thru June 6th not be counted towards the $35,000 if working in public employment?

Thank You,

Is there a letter explaining the change?

Valerie Patterson

Governor Cuomo signed an executive order temporarily suspending the $35,000-a-year earnings limit. Pay from a public employer earned from March 27 through June 6, 2020, will not count toward a retiree’s annual earnings cap. If the order is extended, we will post the information on social media.

While we are undergoing so much anxiety & fiscal uncertainty, it such a reasurrance to know that our pension is being kept safe! Thank you for this!

It’s been mentioned that the new york state teacher’s retirement system may offer a retirement incentive due to the state budget situation. Is there any validity to this? Any time frame set whether it will go through or not?

Thanks and stay well.

The New York State Legislature introduced a bill that would provide a temporary retirement incentive for certain public employees who hold a position represented by one of the recognized collective bargaining units affiliated with the New York State United Teachers (NYSUT) as certified by his or her employer.

Is NYSLRS or NYSTRS supporting this bill?

The New York State Legislature (not NYSLRS) occasionally enacts these retirement incentive programs, which are approved by both houses and signed into law by the Governor. The Retirement System administers programs that are signed into law. We’ll notify your employer if the Legislature makes a State incentive program available.

Will i get a stimulus check

The stimulus payments from the Coronavirus Aid, Relief, and Economic Security (CARES) Act are under the authority of the federal government, not the New York State and Local Retirement System. Please check with the Internal Revenue Service or the U.S. Department of the Treasury for updates regarding your stimulus payment.

Your response to the question about why the Comptroller redirected $50 million dollars to the PPP is completely unacceptable. Mr. DiNapoli has consistently indicated since 2010 that the pension fund would never be used for any purpose but to pay retirees and beneficiaries benefits. The entire membership should be aware of this…and I find it hard to believe that a single member would agree with this…. The taxpayers of the State of New York voted down the referendum on a Constitutional Convention recently to keep the Governor from raiding the pension fund. Now the Comptroller capitulates to political pressure?

The $50 million announcement of this week is not a new investment for the Fund. It is a continuation of an existing program begun in 1987 and in partnership with the NY Business Development Corp., now renamed as Pursuit Lending. It is a positive for New York when we can get a safe, consistent return on an investment and at the same time do something good for our state. We have high investment standards, which is why we are among the best funded of all state pension plans in the nation. For more information about the Fund’s investment strategies, please visit our website at https://www.osc.state.ny.us/pension/index.htm.

Thank you. Your reassurances are welcomed while the Senate Majority Leader contemplates further punishing of “blue” states. As our governor replied, “we are ALL red, white and blue.”

Thank you, I’ve seen where other states in recent years have cut or eliminated pensions for state workers. Am I incorrect in remembering Wisconsin under Gov Walker and cuts in California? If I am I apologize. I’m just wondering where all this money is coming from that is in these stimulus packages. I’m grateful , don’t misunderstand. But there is only so much money to go around. I believe everyone who dedicated their entire working days to an employer, public or private should be entitled to a pension. But that’s not reality. My brother worked for UPS and had his pension slashed by a third. And we all know what happened to the poor folks at St Clare’s hospital. Thank you. Mike

I just read where Mitch McConnell said he would rather see the states go bankrupt than receive anymore federal aid. And not borrow money from future generations to save state pensions. This seems like a new concern that has come about after these prior correspondences.

Under New York State law, Comptroller Thomas P. DiNapoli is the sole trustee of the New York State Common Retirement Fund, which holds the assets of the Retirement System on behalf of members, retirees and beneficiaries. Fund assets cannot be diverted to the State General Fund or used for any other purposes other than paying pension benefits.

Don’t let the fund be raided to make up nys budget deficit due to coronavirus.

Under New York State law, Comptroller Thomas P. DiNapoli is the sole trustee of the New York State Common Retirement Fund, which holds the assets of the Retirement System on behalf of members, retirees and beneficiaries. Fund assets cannot be diverted to the State General Fund or used for any other purposes other than paying pension benefits.

Then why did the comptroller just take $50 million out of the retirement fund?

Whenever prudent, as part of the Fund’s investment strategy, the Comptroller guides the Fund to invest in New York-based business ventures, companies and other programs that spur economic growth and create and retain jobs. The Fund carefully weighs the risk and benefit of every investment, including the Comptroller’s recent announcement of $50 million toward small business relief and job retention. For more information about the Fund’s investment strategies, please visit our website at https://www.osc.state.ny.us/pension/index.htm.

Investments must be made in America. Communist China should not be an investment. Thank you for what you do to protect American workers and our economy=:)

I planned to send in my retirement papers this before April 1. Should I wait?

We’re still accepting retirement applications by mail, but the best way to apply for retirement is through Retirement Online.

Comptroller DiNapoli would like retirees and future retirees to know that the retirement system is well-funded, and that NYSLRS pensions are safe and will continued to be paid as promised.

Thank you for your good sense and hard work. I recall that your strategy has been to conserve and grow funds but to avoid more risky approaches. I think most of us understand that if in the unlikely event our fund is crushed, we won’t be anywhere near the first one.

Providing us with some actual numbers would be nice

For updates on the status of the pension fund, please visit the NYS Common Retirement Fund page.

If you’re asking for statistics on NYSLRS retirees, you can find information in this blog post.

THANK YOU GOD BLESS ALL OF US

NYS Comptroller Thomas DiNapoli and NYSLRS staff,

Thank you for your great work. You provide us with unsurpassed excellence in safeguarding our pension benefits.

Steven Recchia

Thank you for the update. One less thing to reduce the anxiety during these difficult times

There is no doubt the pension system of NY and all state and local governments will be very challenged in the years ahead, given the large drop in planned investment performance. All investments have been hit hard, with many seeing their defined contribution retirement funds decrease dramatically. How will the State and local governments make up for this difference and ensure their pension funds remain solvent? In a time ahead of potential great economic hardships, all options must be on the table. The thought of large property tax increases, to makeup large pension liability shortfalls, is unfathomable.

A very concerned tax payer.

No one knows how long the situation will last, but according to Comptroller DiNapoli, the pension fund’s sole trustee, “The state’s pension fund also faces challenges. Financial markets remain in turmoil as we near March 31, when we calculate the fund’s year end value. Fortunately, our state’s retirement system is well-funded. I want to assure the more than one million men and women, who rely on the state pension fund for retirement security, that we are well-positioned to weather the ongoing volatility. To our retirees, your pensions are safe and we will continue to pay your benefits as promised.

“We take a conservative approach to investing, focused on sustained, long-term results. For some time, we’ve been making adjustments in expectation of a downturn in the economy. We’re actively managing through these difficult times and are confident the markets will ultimately recover.”

Increases in percentages by working employees contributions has been done and may be again as well as other revenue increases. The employees that gave the best working years of their lives (35 more for many) to the people of NYS at a reduced salary compared to the equivalent private sector occupation, often did so for the added security their guaranteed pension offered. When others received higher % raises or enhanced health benefits this promise of one day receiving their steady income from a pension kept them in their jobs. Whatever it takes for the sitting government officials and the working tax payers of NYS to continue to uphold these promises made must be done.

If this were to be compromised, retirees such as a neighbor of mine, who recently passed away in his 90’s and was barely making it would have suffered terribly. He was living on his state pension for nearly 30 years and without a living wage COLA increase over all of those decades. After over 40 years of service in a position that wasn’t by any imagination a high paying job, his only solace was his meager pension.

Now returning to present circumstances, investing in socially preferred agenda driven stocks etc should not have been nor should it EVER be a part of any calculation as it has been done recently.

Every taxpayer and pensioner should have confidence that their hard earned dollars are being invested with a clear eye towards the best possible return regardless of the currently serving political preferences of any comptroller or other influences.

To deny us having our money invested in a highly profitable business or and entire industry because it’s “offensive” to any group is a recipe for eventually limiting options to narrow and rare pile of ”risks” that everyone agrees are socially, morally, politically, etc etc etc agreeable.

Abortion, Guns, Religion, Gender, Race, …. and a myriad other worthy causes deserve all of participation, our FULL ATTENTION, support, protection, and passionate input as they are discussed and debated.

However any legally operating investment opportunity should be “on the table” in contrast to a growing list of uncomfortable current issues causing our states elected but still OUR employees to blacklist certain options because THEY are looking to garner favor with their electorate at the expense of our money earning the highest possible return.

Very long response. But you missed the mark on one critical comparison: salaries over the past decade , if not more, have more than come into parity when comparing these jobs to jobs in the ‘private sector’. Then, there’s a lifetime benefit in retirement of platinum HC at zero cost. The math just does not add up any longer, especially in very tough economic times. It is an unsustainable system.

What everyone in one of these jobs fails to realize, is that for a private sector employee to have a similar retirement ‘nest egg’, they would need to put aside probably 50%-60% of the “much higher annual salary they receive” for about 30 years in order to have the same funds available in retirement. So that right there erases the argument that public workers have had to endure much lower salaries, just so that they can enjoy a pot of gold at the end of the rainbow. The “salary” comparison must take into account the persons full compensation package, not just take home weekly wages.

Not to mention, how does a private sector person plan to retire in their mid 50’s, and then afford to buy health insurance for 10 years at a cost of $1,700 per month?

When clear facts are presented, the situation is obvious.

thank you all for your hard work and dedication.

Thank you! This is very reassuring!

Any talk about an early retirement incentive? I’m over 60 and I am considered essential. It’s scary.

We understand your uneasiness. However, at this time, we’re not aware of any discussions about statewide retirement incentives. The New York State Legislature (not NYSLRS) occasionally enacts these retirement incentive programs, which are approved by both houses and signed into law by the Governor. The Retirement System administers programs that are signed into law. We’ll notify your employer if the Legislature makes a State incentive program available.

Yesterday I heard that a bill was just written (subject to being passed by the houses etc) regarding a new york state teacher’s retirement incentive. Does anyone have any info?

It is the State Legislature (not NYSLRS) that occasionally enacts these retirement incentive programs, which are approved by both houses and signed into law by the Governor. The Retirement System administers programs that are signed into law. We’ll notify your employer if the Legislature makes a State incentive program available.

Thank you for your reassurance.

Thank you for the reassurance

Why would ANYBODY NOT HAVE DIRECT DEPOSIT ???

TY for assuring us – it is one important piece to relieve some of the stress we are facing.

Yes thank you for the reassurance!

Yes we thank you much.

Thank you for the reassurance and all the work you do for our state.