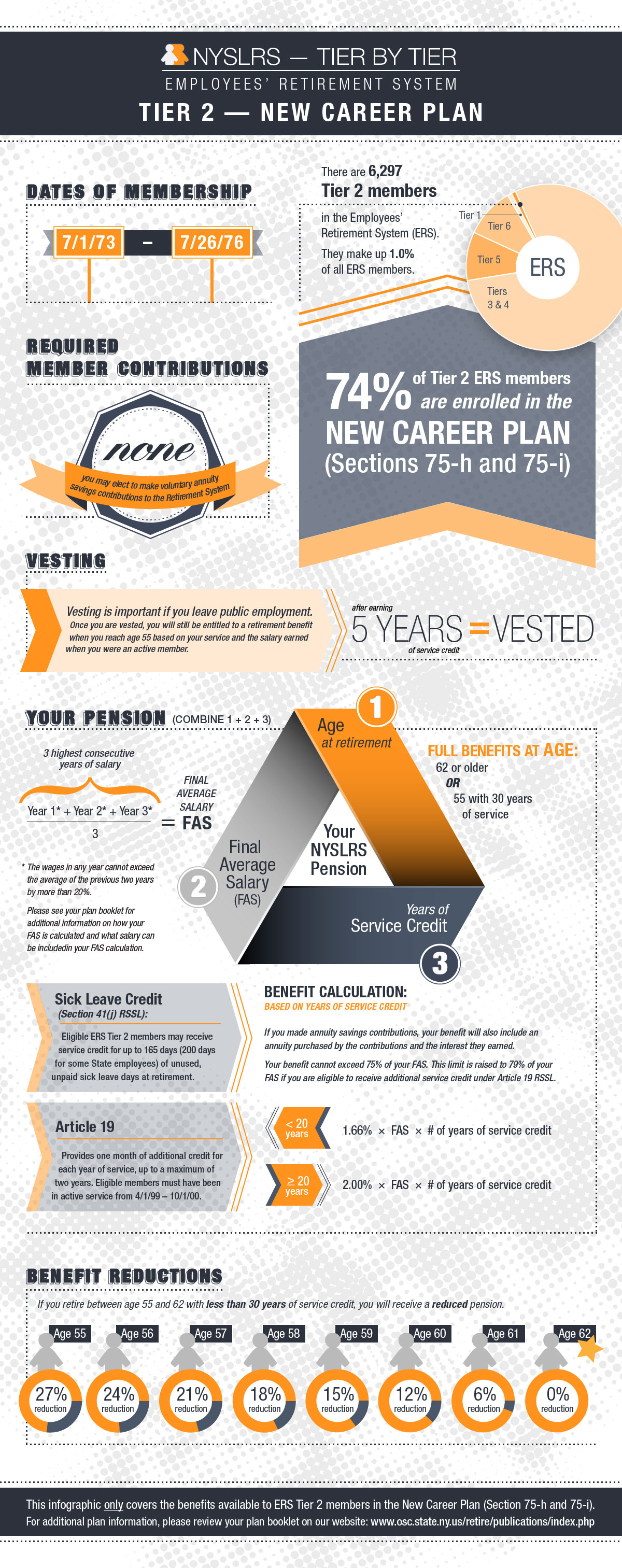

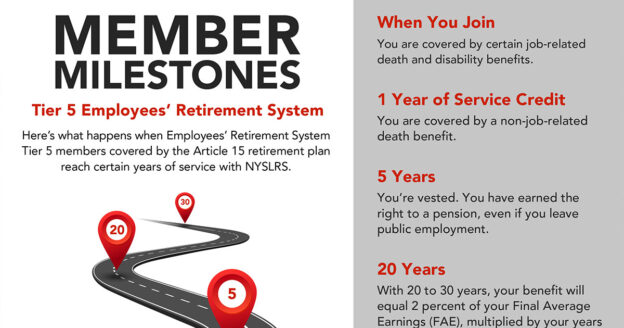

If you joined the Employees’ Retirement System (ERS) on or after January 1, 2010, but before April 1, 2012, you are a Tier 5 member. Let’s look at the milestones you will pass over the course of your public service career and how they will affect your benefits.

Why Milestones Matter

As a NYSLRS member, you earn service credit for your paid public employment. Generally, one year of full-time work equals one year of service credit. Certain amounts of service are milestones because they affect the benefits you receive and how your pension will be calculated. A better understanding of when they occur and how they change your benefits will help you plan for retirement.

Your milestones depend on your tier and your retirement plan. Most ERS Tier 5 members will retire under the Article 15 retirement plan. Some ERS Tier 5 members, such as deputy sheriffs and state corrections officers, are in special plans. You can find information for the Article 15 plan and other Tier 5 plans in your NYSLRS retirement plan publication.

Major Milestones for Tier 5

Here are some important milestones for Tier 5 members in the Article 15 retirement plan:

- With ten years of service credit, you can apply for a non-job-related disability benefit if you are permanently disabled and cannot perform your duties because of a physical or mental condition.

- With ten years of service credit, your beneficiaries may be eligible for an out-of-service death benefit if you leave public employment and die before retirement.

- Ten years also marks the point when you are no longer able to withdraw your membership and receive a refund of your contributions if you leave public employment.

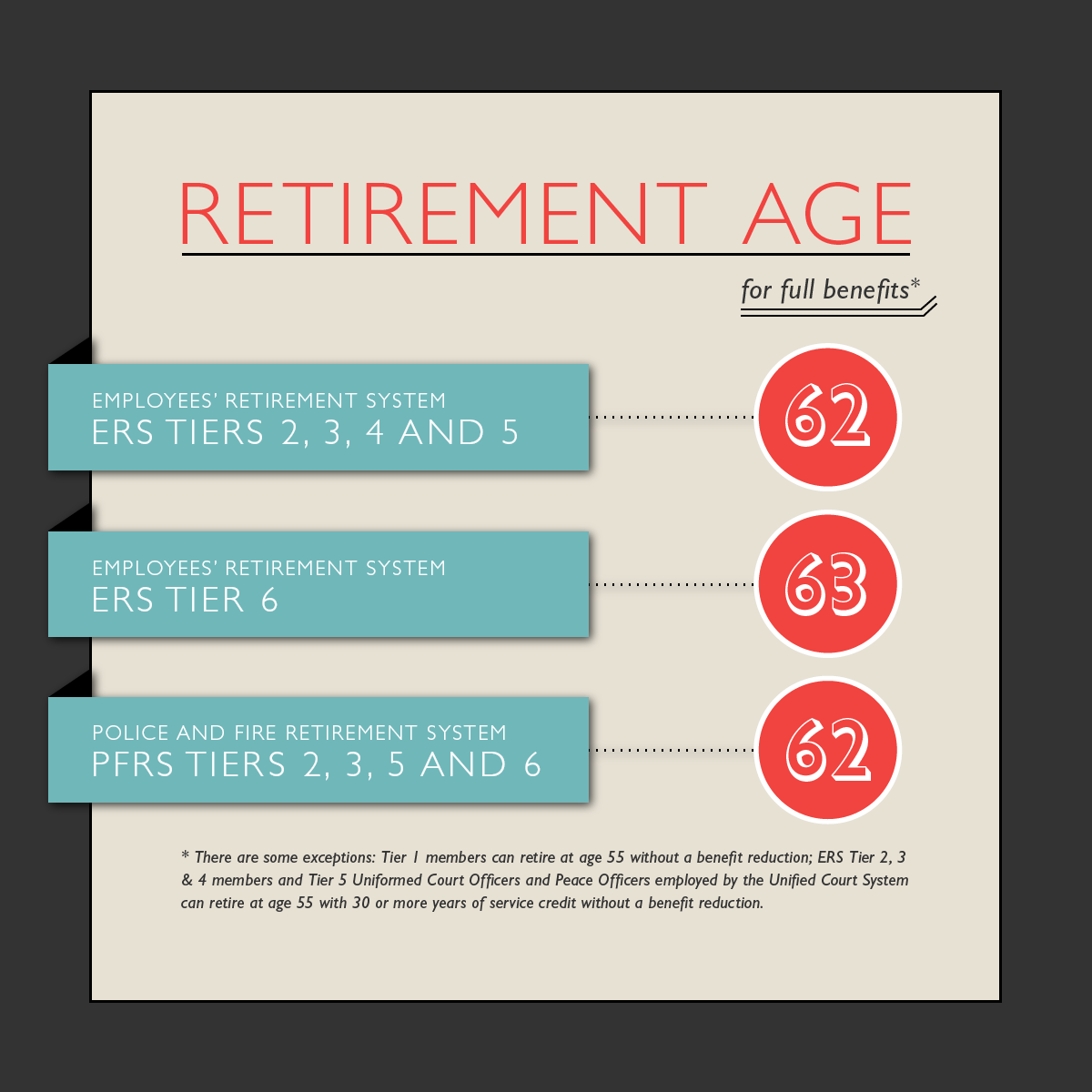

- You are eligible to retire once you are age 55 and have five years of service credit. However, for most Tier 5 members, there would be reductions to your benefit if you retire before age 62.

- You can retire with full benefits at age 62.

- If you retire with fewer than 20 years of service, your pension will equal 1.66 percent of your final average earnings (FAE) for each year of service.

- With 20 to 30 years of service credit, your benefit will equal 2 percent of your FAE for each year of service.

- Then, for each year of service beyond 30 years, you will receive 1.5 percent of your FAE.

Note: The law limits the final average earnings of all members who joined on or after June 17, 1971. For example, for most members, if your earnings increase significantly during the years used in your FAE, it’s possible that some of those earnings may not be used toward your pension. The specific limits vary by tier. Visit our Final Average Earnings page for more information.

The amount of your pension also depends on several factors, including your years of service credit and your age when you retire. Most members can estimate your pension in Retirement Online and enter different retirement dates to see how those choices would affect your benefit. As of April 9, 2022, Tier 5 and 6 members only need five years of service credit to be vested. If you are a Tier 5 or 6 member with between five and ten years of service credit, you can contact us to request a benefit estimate.