Tier 5 and 6 members are subject to limits on the amount of overtime that can be included in their pension. You can earn overtime pay beyond the overtime limit, but it won’t be factored into your pension calculation. And you don’t pay member contributions on overtime pay that is above the limit.

Tier 5 Overtime Limits

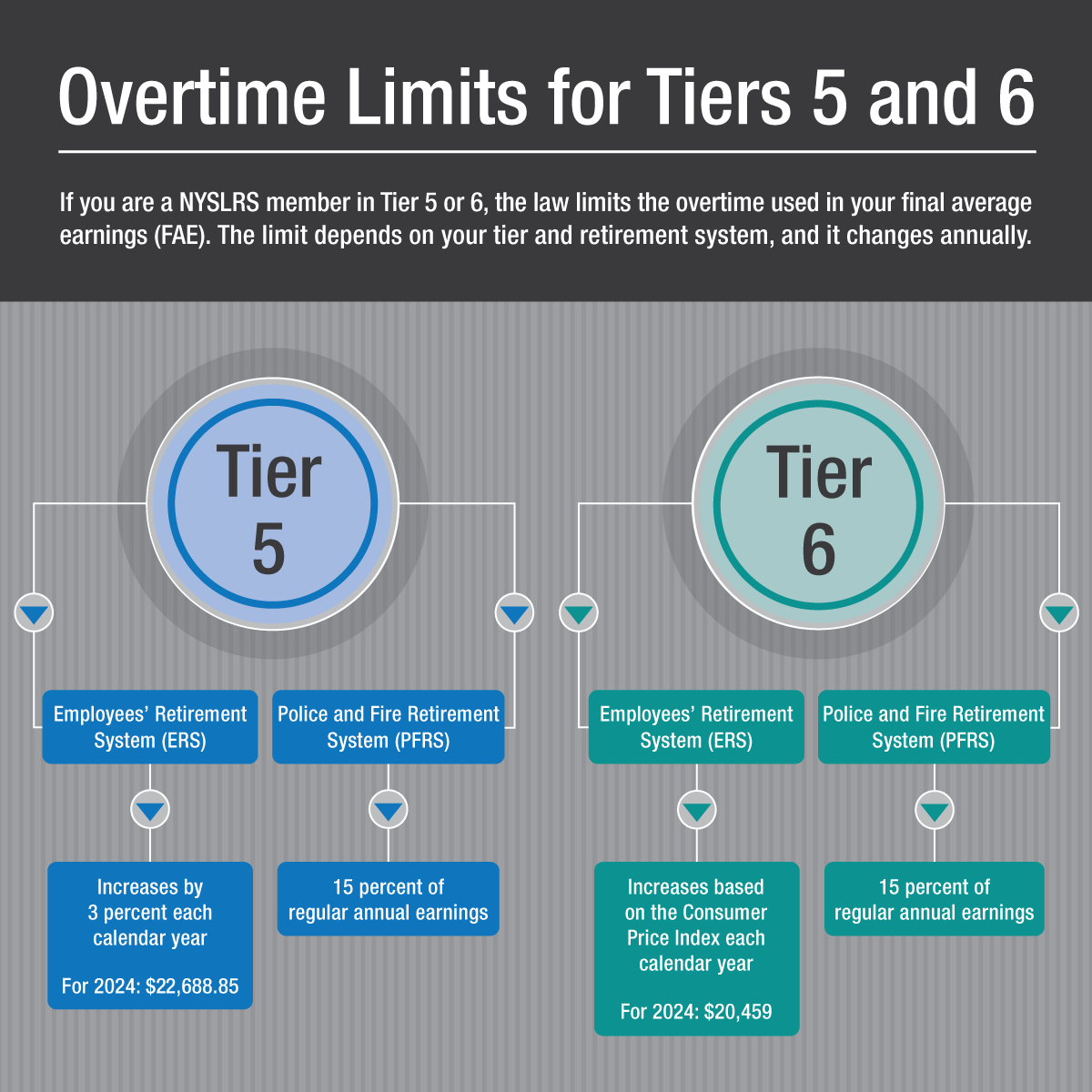

The overtime limit for Tier 5 Employees’ Retirement System (ERS) members increases each calendar year by 3 percent. In 2024, the limit for Tier 5 ERS members is $22,688.85.

For Tier 5 Police and Fire Retirement System (PFRS) members, the overtime limit is 15 percent of your regular earnings each calendar year.

The overtime limit for Tier 6 ERS members increases each calendar year based on the annual increase of the Consumer Price Index (CPI). In 2024, the limit for Tier 6 ERS members is $20,459.

For Tier 6 PFRS members, the overtime limit is 15 percent of your regular earnings each calendar year.

Your NYSLRS pension will be based on your service credit and final average earnings (FAE). Your FAE is the average annual earnings you receive during the period when your earnings are highest (36 consecutive months for Tier 5 and 60 consecutive months for Tier 6). Your FAE will include overtime pay you earned up to each annual limit.

Your FAE may be limited in other ways. For example, for most members, if your earnings increase significantly in the years used for your FAE, some of those earnings might not count toward your pension. The specific limits depend on your tier. Visit our Final Average Earnings page for more information about this limit.

Your retirement plan publication provides specific information about the earnings that will be used to calculate your pension. Visit our website to Find Your NYSLRS Retirement Plan Publication.

Estimate Your Pension in Retirement Online

Most members can create their own pension estimate in minutes using Retirement Online. You can enter different retirement dates to see how those choices would affect your benefit. Sign in to Retirement Online and click the “Estimate my Pension Benefit” button to try it.

When it comes to managing your NYSLRS account, Retirement Online is the fastest way to do it. Skip printing forms, having them notarized and sending them through the mail — when you submit your requests online, NYSLRS has them immediately and your changes will be completed more quickly. It’s convenient, and it’s secure.

Here’s a look at some of the things NYSLRS members (not yet retired) can do online.

View Your Account Information

Sign in to Retirement Online for easy access to key information to help you plan for retirement. On your Account Homepage, you can find your date of membership, tier, retirement plan (which you can use to find your retirement plan publication), estimated total service credit and more.

Change Your Delivery Preference to Email and Help Us ‘Go Green’

Save time and reduce paper waste — help us ‘go green’ by choosing the paperless option. When you choose to receive information from NYSLRS electronically, we will send you an email when important documents and letters are ready to view in Retirement Online.

From your Account Homepage, click the “update” link next to ‘Contact by’ or ‘Member Annual Statement by.’

Choose “Email” from the dropdown menu.

If you choose “Email” as your delivery preference, you will not receive a printed copy in the mail.

Update Your Contact Information

It’s important that we have your current contact information so you receive the news, letters and statements that we send you. You can update your email address, mailing address and phone number in the ‘My Profile Information’ section of your Account Homepage. Just click “update” next to the item you’d like to change. Use a personal email address that you will have access to before and after you retire, rather than a work email address.

View and Update Your Beneficiary

NYSLRS retirement plans provide death benefits for beneficiaries of eligible members who die before retiring. It’s a good idea to review your beneficiaries from time to time to make sure your choices reflect your current wishes. Retirement Online is the fastest way to add or remove beneficiaries or update their contact information. Click the “View and Update My Beneficiaries” button to get started.

Estimate Your Pension

How much will your pension be? It’s an important question as you’re planning for retirement. In just a few steps, most members can estimate their retirement benefit based on up-to-date account information, then save or print the estimate. Entering different dates and comparing the results can help you choose the retirement date that’s right for you. From your Account Homepage, click the “Estimate my Pension Benefit” button.

Apply for a Loan and Manage Loan Payments

It’s easy to apply for a loan in Retirement Online. If you are eligible to take a loan against your retirement contributions, you can see how much you can borrow, your repayment options and whether your loan will be taxable — all before you apply. Click the “Apply for a Loan” button to start an application.

If you have an existing loan, you can click the “Manage My Loans” button to adjust your payment amount or to make an additional one-time payment.

Request Credit for Previous Service

If you worked for a participating public employer before joining NYSLRS, or if you served in the U.S. Armed Forces, you may be able to purchase service credit for that time. Click the “Manage My Service Credit Purchases” button to request credit and upload any supporting documentation.

Purchase previous service credit as soon as possible. It’s cheaper and will make it easier to calculate your final monthly pension payment.

Get Your Member Annual Statement Faster

Your Member Annual Statement can help you understand your benefits. It’s a snapshot of your NYSLRS account based on the information we have on file for you as of March 31 each year, the close of our fiscal year. Statements will be available online in the spring, sooner than printed copies will be mailed — update your delivery preference to “Email” to get notified when it’s available online.

Generate a Mortgage Verification Letter

If you need to provide proof of your NYSLRS account information for a mortgage, you can get your own income verification letter online. From your Account Homepage, in the ‘I want to…’ section at the top right, click the “Generate Income Verification Letter” link. You can print a document that shows your contribution balance, and — if you have an outstanding loan — the date of your last loan, the current balance and the interest rate.

Apply for Retirement

When you are ready to retire, Retirement Online allows you to skip the hassle of mailing paper forms or visiting our office. You can apply for a service retirement benefit, choose your pension payment option, sign up for direct deposit and submit retirement-related paperwork online. A big advantage of applying online is that you don’t have to get anything notarized. Read our blog post about applying for retirement for more information and links to resources.

Other Online Transactions

If you previously were a member of another New York State public retirement system before joining NYSLRS, your service could be recredited and your date of membership and tier restored. You can click the “Reinstate a Previous Membership” button to get started.

If you leave public employment with less than ten years of service credit, you can use Retirement Online to withdraw your membership. However, this will terminate your membership with NYSLRS. If you have any questions, speak with a customer service representative before you submit your withdrawal application. You can message them using our secure contact form.

Brush up on your Retirement System knowledge! Here are 10 things all NYSLRS members should know.

Lifetime Retirement Benefit You are part of a defined benefit pension plan, which provides a lifetime benefit at retirement based on your earnings and years of service.

Qualify for a Retirement Benefit by Becoming Vested Becoming vested is a key milestone in every NYSLRS member’s career. Once you’re vested, you have earned enough service to qualify for a retirement benefit, once you meet the minimum age requirements established by your retirement plan.

Tier Determines Benefits Your tier determines your eligibility for benefits under your plan and how those benefits are calculated.

Conduct NYSLRS Business Using Retirement Online Retirement Online is the fastest and most convenient way to do business with NYSLRS. It only takes a few minutes to open your account. Use Retirement Onlineinstead of calling or mailing for instant access to benefit information and convenient tools to make account changes.

Estimate Pension Using Retirement Online Calculator Most members can use Retirement Online to create benefit estimates based on the most up-to-date information we have on file. You can enter different retirement dates and payment options to see how those choices would affect your benefit.

Use Plan Publication to Learn about Benefits Your retirement plan publication is a comprehensive source for information about your benefits.

Pension Calculated Using Highest Earnings Your final average earnings (FAE) is another major factor in calculating your NYSLRS pension. When we calculate your pension, we find the set of consecutive years (one, three or five, depending on your tier and retirement plan) when your earnings were highest.

Request Past Service Credit Before Retirement Service credit is one of the major factors in calculating your NYSLRS pension. You earn a year of service credit for each year of full-time employment with a participating employer. In some cases, you may also be able to request additional credit for past service.

NYSLRS Membership Includes Death and Disability Benefits NYSLRS membership provides more than just retirement benefits. If you become seriously ill or injured, you may be eligible for a disability benefit. And, you may also be eligible to leave a beneficiary a death benefit if you die while working for a public employer.

Best-Funded, Best-Managed The New York State Common Retirement Fund holds and invests the assets of NYSLRS on behalf of members, retirees and their beneficiaries and continues to be one of the best-funded and best-managed public pension funds in the nation. Comptroller Thomas P. DiNapoli is the administrative head of NYSLRS and trustee of the Common Retirement Fund.

NYSLRS is one of the largest public retirement systems in America, serving more than 1.2 million members, retirees and beneficiaries. Read A Look Inside NYSLRS to learn more about your retirement system.

Becoming vested is a crucial milestone for NYSLRS members. It means you have earned enough service to qualify for a retirement benefit once you meet the age or service requirements established by your retirement plan. Vesting is automatic — you don’t have to fill out any paperwork to become vested.

Years of Service Credit to Become Vested

NYSLRS members in Tiers 2 – 6 need five years of service credit to be vested.

If you work part-time, or if you have an unpaid leave of absence, it will take longer to become vested. For example, if you work half-time, you earn six months of credit toward vesting for each year on the job.

Note: Previously, Tier 5 and 6 members needed ten years of service to be eligible for a service retirement benefit. However, as of April 9, 2022, these members only need five years of service credit to be vested. The new law did not change benefit rules such as how long members must contribute, pension benefit calculations, the full retirement age, reductions to retire early or the cost to purchase previous service.

Applying for Retirement

Vesting is automatic, but you will need to apply for retirement to receive your pension — NYSLRS will not pay out your pension benefit unless you apply for it.

Pension eligibility requirements and benefit calculations depend on your tier and retirement plan. To find your tier and retirement plan, sign in to your Retirement Online account and go to the ‘My Account Summary’ section. Once you know your tier and retirement plan, you can find your retirement plan publication for comprehensive information about your benefits and filing instructions.

A lot can change in our lives, and sometimes people switch jobs or professions during their career. Perhaps you were a teacher, and you recently began working for New York State. Or maybe you had a job with New York City, and you took a position with a municipality outside of the city. If you are an active member of more than one public retirement system in New York State, you may have the option of transferring that membership to NYSLRS and receiving credit for that service.

Considering Service Credit

Service credit is a factor in calculating a NYSLRS pension benefit, so increasing your service credit will generally increase your pension benefit.

In some cases, transferring membership may not be beneficial. For example, if you are in a retirement plan that allows for retirement after 20 or 25 years of service (regardless of age), your service usually must be in specific job titles to be creditable toward your pension benefit. If you are in one of these plans, find your retirement plan publication to learn what service is creditable.

If you have questions, contact a customer service representative before you apply to transfer a membership. You can message them using our secure contact form.

Transferring Membership

Members who are transferring membership to NYSLRS must:

Be on the payroll in a job that is covered by NYSLRS;

No longer work in the job that was covered by the other retirement system; and

Still be an active member of the other system (off payroll for that job, but your membership in the other system has not been terminated or withdrawn).

To transfer a membership to NYSLRS, you first must submit a transfer request to your other retirement system. When we receive your membership information from the other retirement system, we will compare your date of membership in NYSLRS with your date of membership in the other system. When the transfer is complete, your date of membership will be the earlier of the two dates. If applicable, your tier will change.

If You Need to Transfer to Another System

You can submit an online request to NYSLRS to transfer your membership from NYSLRS to another New York State public retirement system:

So how do we determine service credit for school employees?

Service Credit for School Employees

As a member, you receive service credit for paid public employment beginning with your date of membership. That credit is based on the number of days you work, which your employer reports to us.

If you’re working full-time, you receive one year of service per school year, even if you only work 10 months of the year.

For part-time work, your employer calculates days worked by dividing the number of hours worked by the hours in a full-time day. The number of hours in a full-time day is set by your employer (between six and eight hours). So, for example, if a 40-hour work week is considered full-time for your employer, and you work 20 hours a week for a given school year, you will receive half a year of service credit.

Calculating Service Credit

Usually, a full-time, 10-month school year is at least 180 days. However, depending on your employer, a full academic year can range from 170 days to 200 days. Whether you work full- or part-time, your service is based on the length of your school year:

For all BOCES and school district employees, as well as teachers working at New York State schools for the deaf and blind: Number of days worked ÷ 180 days

For college employees: Number of days worked ÷ 170 days

For institutional teachers: Number of days worked ÷ 200 days

Check Your Service Credit

You can sign in to Retirement Online and find your current estimated service credit listed on your Account Homepage under ‘My Account Summary.’

If you’re not sure whether you’re earning full-time or part-time service, you can check your most recent Member Annual Statement to see how much service you earned over the past fiscal year. To view your most recent Statement, sign in to Retirement Online. From your Account Homepage, click the “View My Member Annual Statement” button under ‘My Account Summary.’ If you are receiving full-time service, it will say “1.00 Years” for service credited from 4/1/2022 – 3/31/2023. A reminder: the total credited service you will see listed on your Statement was as of March 31, 2023.

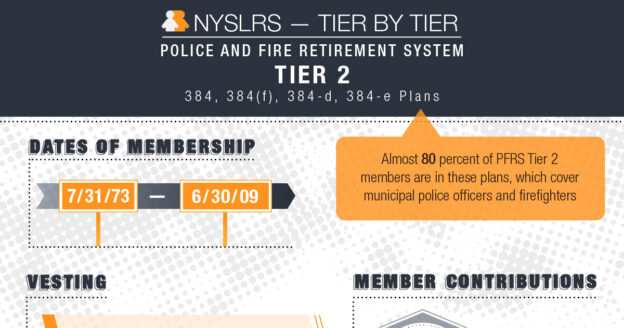

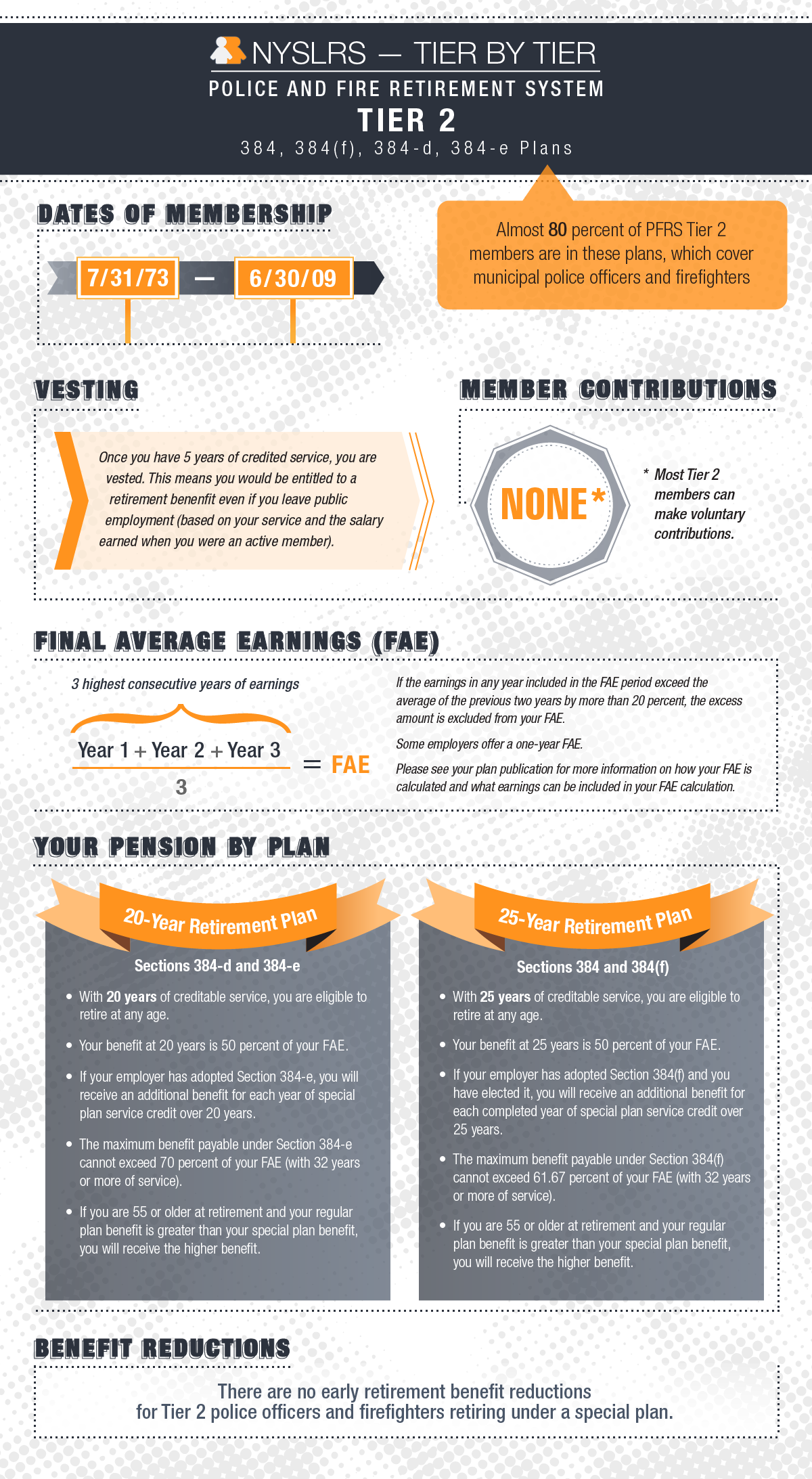

When you join the New York State and Local Retirement System (NYSLRS), you’re assigned a tier based on the date of your membership. This post looks at Tier 2 members of the Police and Fire Retirement System (PFRS).

Your tier determines such things as your eligibility for benefits, the calculation of those benefits, death benefit coverage and whether you need to contribute toward your benefits.

PFRS has five tiers. Almost half of PFRS members are in Tier 2, which began on July 31, 1973, and ended on June 30, 2009. Most are in special retirement plans that allow for retirement after 20 or 25 years, regardless of age, without penalty.

The special plans that cover most police officers and firefighters fall under Sections 384, 384(f), 384-d, and 384-e of Retirement and Social Security Law. You can sign in to Retirement Online to find your benefit plan, which is listed under ‘My Account Summary.’

Where to Find PFRS Tier 2 Information

Whether you’re in one of the retirement plans described in this post or another retirement plan, we encourage you to visit our website to find your NYSLRS retirement plan publication. It’s a comprehensive description of the benefits you’re entitled to receive as a PFRS member.

You can check your service credit total and estimate your pension using Retirement Online. Most members can use our online pension calculator to create an estimate based on the salary and service information NYSLRS has on file for them. You can enter different retirement dates to see how your choices would affect your potential benefit.

Members may not be able to use the Retirement Online calculator in certain circumstances, for example, if they have recently transferred a membership to NYSLRS, if they are a Tier 6 member with between five and ten years of service, or if they have worked for multiple employers and were covered by different retirement plans. These members can contact us to request an estimate or use the “Quick Calculator” on our website. The Quick Calculator generates estimates based on information you provide.

Service credit is one of the major factors in calculating your NYSLRS pension. You earn a year of service credit for each year of full-time employment with a participating employer. In some cases, you may also be able to request additional credit for past service, which could increase your pension amount.

You can request credit for past service if you:

Worked for a participating employer before joining NYSLRS;

Worked for a public employer that later participated in NYSLRS; or

Received an honorable discharge from active military duty.

In most cases, you have to pay to receive additional service credit. The sooner you purchase your credit, the less it will generally cost. You must apply for any additional service credit that you wish to receive before you retire. After you apply, we’ll determine whether you’re eligible for the credit and how much it would be.

Credit for Previous Public Employment

Additional service credit includes work for an employer who later joined NYSLRS, or for public employment before you became a NYSLRS member.

Example: You worked at the town library while going to school and, as a part-time employee, you chose not to join NYSLRS. When you graduated and took a full-time job at the Town Supervisor’s office, you were required to join. You can request credit for the part-time service at the library.

When you apply, you’ll be asked for the name of the employer and the approximate dates you worked there. We encourage you to submit any proof you may have of your previous service. We will also reach out to your former employer, but you may be able to expedite the process by providing payroll records such as W-2 forms or pay stubs to NYSLRS when you apply.

You must earn two years of service credit as a member before additional service can be credited to you.

Military Service Credit

If you served in the U.S. armed forces, you may be eligible to purchase credit toward your retirement for your military service, regardless of whether your military service was before or after you joined NYSLRS.

There are different sections of the law that allow credit for military service. The amount of military service credit you can receive, and the cost (if any), will vary depending on which section of the law allows the credit. Reserve and National Guard service may qualify if it’s considered active duty.

For certain military service, you must have five years of member service credit before you can apply.

How to Request Additional Service Credit

You can apply for additional service credit and military service credit in Retirement Online. Sign in to your account, scroll down to the ‘My Account Summary’ section of your Account Homepage and click the “Manage My Service Purchases” button, then click “Request Additional Service Credit.” If you are applying for military service credit, select “Article 20 Military” when asked for your employer.

There may be other ways to increase your retirement service credit. If you had a previous membership in a New York State public retirement system and it was terminated, you may be able to reinstate your membership. If you still have an active membership in another public retirement system, but you are no longer working for the employer that participates in that retirement system, you may be able to transfer that membership to NYSLRS.

A word of caution — there are certain situations where purchasing additional service credit will not increase your pension. For example, special retirement plans for police officers and firefighters allow retirement after 20 or 25 years of service regardless of age, but not all types of public employment count toward the 20 or 25 years in these plans. Contact us if you have questions.

For more information about purchasing additional credit:

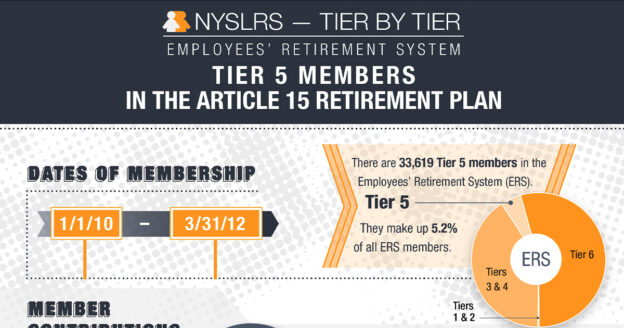

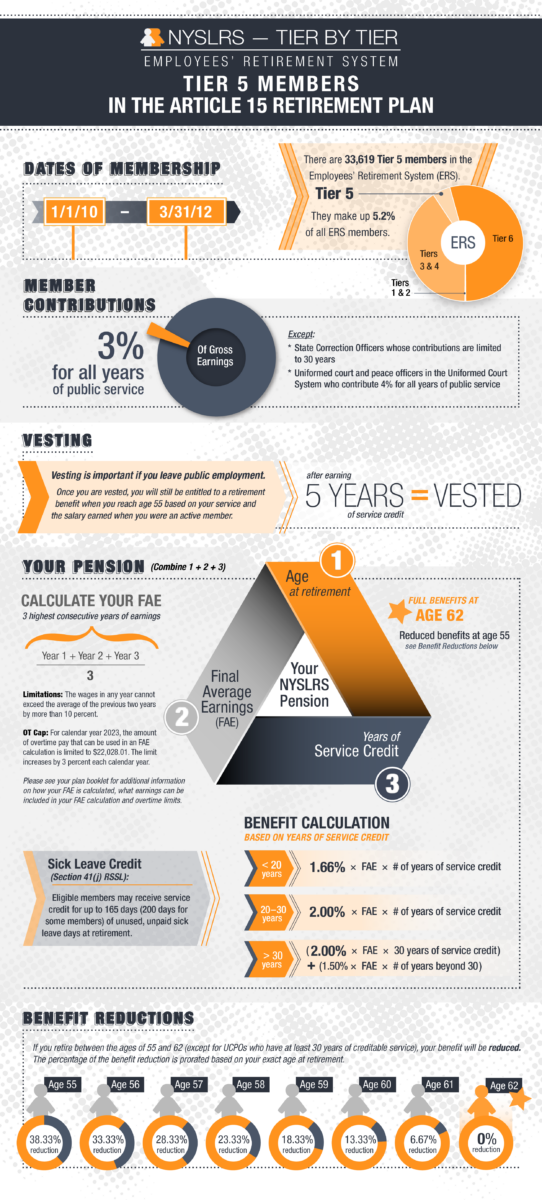

When you joined the New York State and Local Retirement System (NYSLRS), you were assigned a tier based on the date of your membership. This post looks at Tier 5 members of the Employees’ Retirement System (ERS).

Your tier determines such things as your eligibility for benefits, the calculation of those benefits, death benefit coverage and whether you need to contribute toward your benefits.

ERS has six tiers. Anyone who joined from January 1, 2010 through March 31, 2012 is in Tier 5. There were 33,619 ERS Tier 5 members as of March 31, 2022, representing 5.2 percent of ERS membership.

Most ERS Tier 5 members (unless they are in special retirement plans) retire under the Article 15 retirement plan. Check out the graphic below for the basic retirement information for Tier 5 members in this plan.

If you retire with less than 20 years, the benefit is 1.66 percent of your final average earnings (FAE) for each year of service. If you retire with 20 to 30 years, the benefit is 2 percent of your FAE for each year of service. For each year of service beyond 30 years, you will receive 1.5 percent of your FAE. For example, with 35 years of service, you can retire at 62 with 67.5 percent of your FAE.

Where to Find More ERS Tier 5 Information

For more information about ERS Tier 5 membership, find your NYSLRS retirement plan publication. It’s a comprehensive description of the benefits provided by your specific plan.

You can check your service credit total and estimate your pension using Retirement Online. Most members can use our online pension calculator to create an estimate based on the salary and service information NYSLRS has on file for them. You can enter different retirement dates to see how your choices would affect your potential benefit.

Members may not be able to use the Retirement Online calculator in certain circumstances, for example, if they have recently transferred a membership to NYSLRS. These members can contact us to request an estimate or use the “Quick Calculator” on our website. The Quick Calculator generates estimates based on information you provide.

For information about other tiers, our series NYSLRS – One Tier at a Time gives you a quick look at the benefits for other tiers in both ERS and the Police and Fire Retirement System.

*Uniformed court officers or peace officers employed by the Unified Court System that have at least 30 years of credit may retire with a full benefit as early as age 55.

Retirement law can be confusing. Sometimes a small misunderstanding can have a big impact on your benefit. That’s why it’s important to correct some common retirement myths. Here are the top five:

Retirement Myth #1

My NYSLRS contributions go into a personal 401(k)-style savings account that I will get when I retire.

NYSLRS is a defined benefit plan. Your pension will be based on your earnings and years of service — it will not be based on your contributions.

Retirement Myth #2

If I work for more than one NYSLRS participating employer, the service credit from both will count toward my pension benefit.

It depends. You can only earn one year of service credit in a 12-month period. If you work part-time for two participating employers, you would receive credit toward retirement from both, up to the maximum of one year. However, if you already work full-time for one NYSLRS employer plus you work part-time for another employer, your part-time job won’t increase your retirement service credit. Also, if you are a full-time employee of a school district, you won’t earn extra service credit if you work during the summer.

Retirement Myth #3

NYSLRS administers health insurance coverage for its retirees.

NYSLRS does not administer health insurance programs. We may deduct premiums from a retiree’s monthly pension benefit to pay for health insurance coverage if their former employer instructs us to do so, but we can’t answer questions about coverage or changes in premium amounts.

The New York State Department of Civil Service administers the New York State Health Insurance Program (NYSHIP) for New York State retirees and some municipal retirees. If you are still working, your employer’s human resources (personnel) office should be able to answer your questions about post-retirement coverage.

Retirement Myth #4

I can take out a NYSLRS loan after I retire.

You need to actively work for New York State or a participating employer to borrow against your retirement contributions. NYSLRS loans are not available to retirees.

Retirement Myth #5

If I’m vested and no longer working for a public employer, NYSLRS will automatically start paying my pension as soon as I’m eligible.

Your pension is not automatic. You must apply for retirement 15 to 90 days before your retirement date. Your retirement date is up to you. Most NYSLRS members can begin collecting their pension as early as age 55. If you retire between age 55 and your full retirement age (62 of 63, depending on your tier and plan), you may face a permanent benefit reduction. If you have left public employment though, your benefit won’t increase after you reach full retirement age, so delaying retirement beyond that point can cost you money.

You can find more answers about your NYSLRS benefits in your retirement plan publication. If you have account-specific questions, please message our customer service representatives using our secure contact form.

While most New York teachers and administrators are in the

While most New York teachers and administrators are in the