We accumulate a lot of important documents over a lifetime — things such as birth certificates, diplomas, deeds, wills, insurance policies and more. If you’re like many people, you may have papers stuffed in drawers, filing cabinets or boxes in the attic. If you need an important document, will you be able to find it? What’s more, when you pass away, will your loved ones be able to find what they need?

Organize Your Important Documents

Important documents should be kept in a secure but accessible place in your home. This includes personal documents, such as your passport, birth certificate, marriage certificate, will and burial instructions. You should also include information about your NYSLRS retirement benefits, income taxes, bank accounts, credit cards and online accounts. Important contact information, such as the names and phone numbers of your attorney, accountant, stockbroker, financial planner, insurance agent and executor of your will should also kept in a secure location.

Our fillable form, Where My Assets Are, can help make organizing your important documents a little easier. It will help you or your loved ones locate these documents when they are needed. It’s a good idea to review and update this information regularly.

Be aware that a safe deposit box may be sealed when you die. Don’t keep burial instructions, power of attorney or your will in a safe deposit box, because these items may not be available until a probate judge orders the box to be opened. However, a joint lessee of the box, or someone authorized by you, would be permitted to open the box to examine and copy your burial instructions.

Review Death Benefits and Beneficiary Designations

Depending on your tier and retirement plan, your beneficiaries may be eligible to receive a death benefit. Visit our member and retiree death benefit pages for more information.

Then, sign in to your Retirement Online account to review your named beneficiaries and update their contact information if needed. From your Account Homepage, click “View and Update My Beneficiaries” to get started.

Please note, when a NYSLRS member or retiree dies, it is important that survivorsreport the death to NYSLRSas soon as possible. Before any death benefits can be processed or paid, NYSLRS will need an original, certified death certificate.

A good estimate of your post-retirement income is essential for effective retirement planning. But gauging your income can be tricky when it comes from multiple sources. Fortunately, there are a variety of online calculators that can help you get started.

NYSLRS Benefit Calculator

Most NYSLRS members can quickly create a pension estimate using Retirement Online. Your estimate will be based on the most up-to-date account information we have on file for you. You can enter different retirement dates to see how those choices would affect your benefit and adjust your earnings or service credit if you anticipate a raise or plan to purchase past service.

If you are saving for retirement, a simple savings calculator can give you an idea of how your money can grow over the years. However, simple calculators like this assume a fixed amount of savings each month. Most people increase their retirement savings as their income grows.

Savings withdrawal calculators are designed to help determine how much savings remains after a series of withdrawals. These are especially helpful tools to use when trying to determine how long your retirement savings will last, based on a starting amount, how much you expect to withdraw, how often and some other factors.

How Much Do You Need?

Now that you’ve estimated your potential sources of retirement income, it’s important to understand your anticipated expenses in retirement. Our Income and Expenses Worksheet can help you create a post-retirement budget.

Think of retirement security as a three-legged stool, with your NYSLRS pension, social security benefit and retirement savings working together to provide financial stability. Your NYSLRS pension is a defined benefit, or traditional pension, that will provide you with a monthly payment for the rest of your life. Having a retirement savings account can give you more flexibility to do the things you want to do, or provide a source of cash in case of an emergency. Start saving for retirement if you haven’t already, or give your retirement savings a boost.

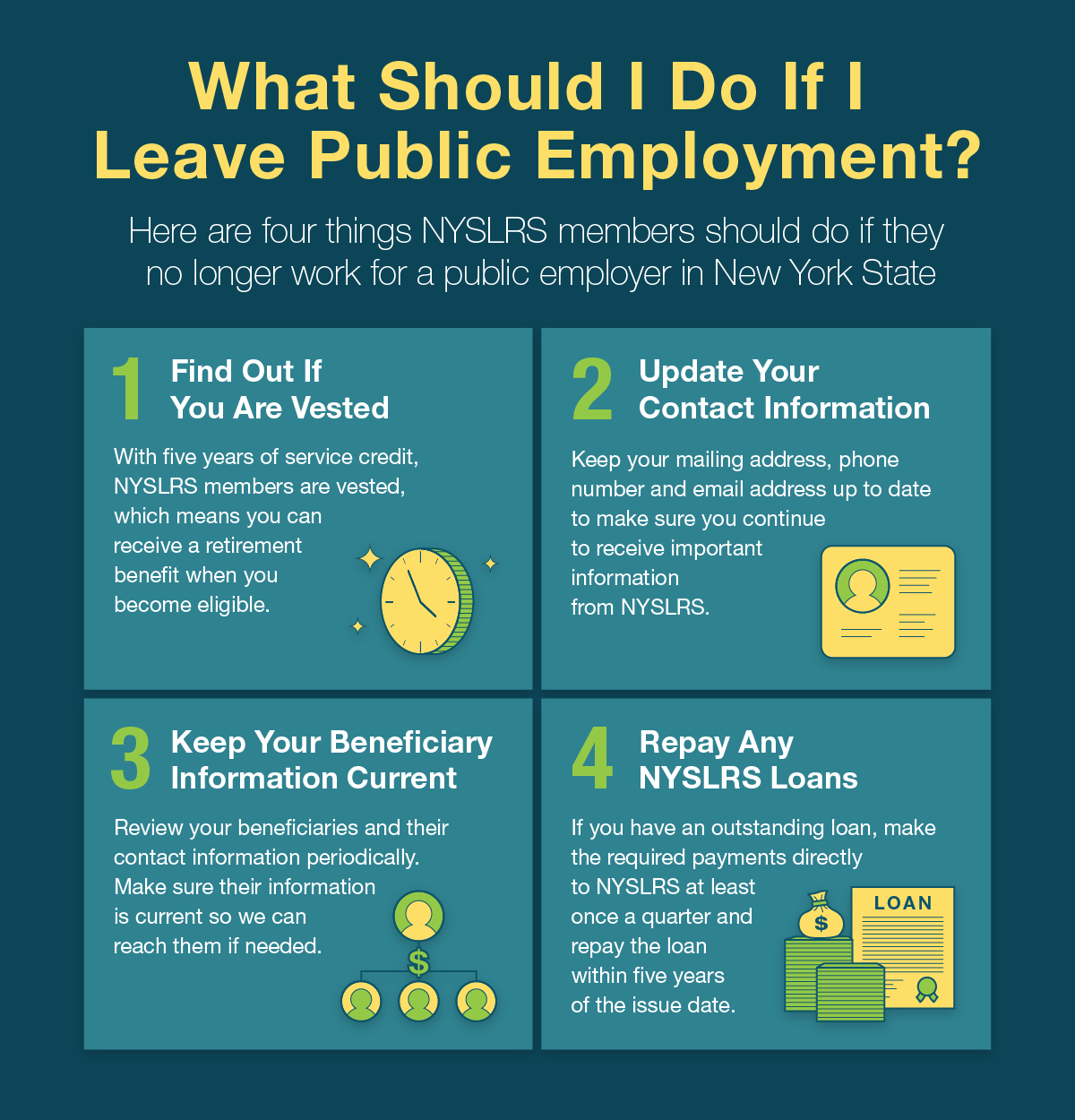

It may not come up during your career, but if you leave public employment before you are eligible to retire, you should know what happens with your NYSLRS membership and benefits. Your options will depend on how many years of service you have. It’s also important to keep your account information up to date. If you remain a member of NYSLRS after you leave public employment, you can regularly review your account information and keep it up to date by using Retirement Online.

If you have 5 or more years of service when you leave public employment, and you leave public employment before you are eligible to retire, you can receive a vested retirement benefit when you become eligible.

If you leave with between five and ten years of service, you can either remain a member and receive a vested retirement benefit when you become eligible or terminate your membership and receive a refund of your contributions.

If you leave with more than ten years of service, you cannot withdraw your NYSLRS membership and you can receive a vested retirement benefit when you become eligible and apply.

If you leave with less than ten years of service, you can end your membership and receive a refund of your contributions.

Keep Your Contact Information Updated

It’s important to make sure we have your current mailing address, phone number and personal email address, and let us know about any future changes. That way, you won’t miss important information from us, such as your Member Annual Statement.

To update your contact information, sign in to Retirement Online. Go to ‘My Profile Information,’ find your address, phone number or email address under ‘My Profile Information’ and click “update.”

Keep Your Beneficiaries Updated

If you leave public employment, your beneficiaries may still be eligible for a death benefit, so you should review your beneficiary designations periodically. Sign in to Retirement Online, go to the ‘My Account Summary’ area of your Account Homepage and click “View and Update My Beneficiaries.” Your beneficiary changes will be considered filed on the day you submit them.

Repay Any NYSLRS Loans

If you leave public employment, you will no longer be able to pay off your NYSLRS loans by payroll deduction. If you have any outstanding NYSLRS loans, you must make payments directly to NYSLRS at least once every three months and repay your loan within five years of when it was issued, or you will default on the loan. Defaulting on a loan may carry considerable tax consequences: You’ll need to pay ordinary income tax and possibly an additional 10 percent penalty on the taxable portion of the loan. You can make loan payments to NYSLRS via Retirement Online.

You aren’t eligible to take a new NYSLRS loan once you are off the public payroll.

Receiving a Vested Retirement Benefit

If you are vested, once you reach retirement age, you can receive a lifetime pension based on your salary and service from when you were working in public employment. It’s your responsibility to apply for retirement — NYSLRS will not pay out your pension benefit unless you apply for it.

The earliest date you can receive your retirement benefit depends on your tier and retirement system.

Tier 1 and 2 members are eligible for a vested retirement benefit as early as the first of the month following your 55th birthday.

Tier 3, 4 and 5 members and Employees’ Retirement System (ERS) Tier 6 members are eligible for a vested retirement benefit as early as your 55th birthday.

Police and Fire Retirement System (PFRS) Tier 6 members are eligible for a vested retirement benefit on your 63rd birthday.

For most members, however, if you retire before your full retirement age, you would face a permanent early retirement benefit reduction. The full retirement age is 62 for Tier 1 – 5 members, and age 63 for ERS Tier 6 members and off-payroll PFRS Tier 6 members.

Most members can estimate your pension amount using the benefit calculator in Retirement Online. Sign in to your Retirement Online account, go to the ‘My Account Summary’ area of your Account Homepage and click the “Estimate my Pension Benefit” button. You can also apply for your retirement benefit using Retirement Online.

If You Leave Public Employment with Less than Ten Years of Service

With less than ten years of service credit, you can choose to end your membership and request a refund of your contributions. If you withdraw your contributions, however, you will no longer be eligible to receive a pension benefit. You can withdraw by signing in to Retirement Online, going to the ‘My Account Summary’ area of your Account Homepage, and clicking “Withdraw My Membership.”

You cannot withdraw from NYSLRS once you have ten years of service credit.

(Note: Tier 1 and 2 members and PFRS Tier 3 (Article 11) members covered by a non-contributory retirement plan can make voluntary contributions. These members can withdraw their voluntary contributions without ending their membership. Contact us if you have questions.)

If you have less than five years of service credit (aren’t vested) and don’t withdraw your contributions, they will continue to earn 5 percent interest for seven years. After seven years off the public payroll, your membership ends automatically, and your contributions will be deposited into a non-interest-bearing account until you withdraw them.

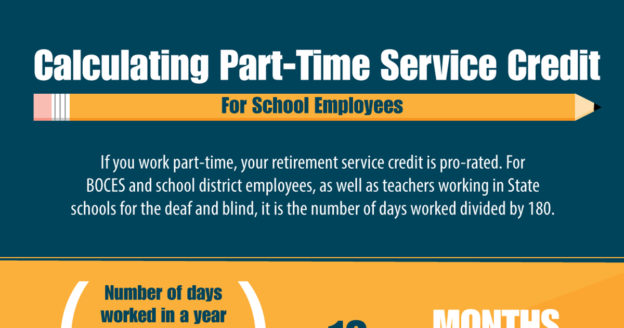

So how do we determine service credit for school employees?

Service Credit for School Employees

As a member, you receive service credit for paid public employment beginning with your date of membership. That credit is based on the number of days you work, which your employer reports to us.

If you’re working full-time, you receive one year of service per school year, even if you only work 10 months of the year.

For part-time work, your employer calculates days worked by dividing the number of hours worked by the hours in a full-time day. The number of hours in a full-time day is set by your employer (between six and eight hours). So, for example, if a 40-hour work week is considered full-time for your employer, and you work 20 hours a week for a given school year, you will receive half a year of service credit.

Calculating Service Credit

Usually, a full-time, 10-month school year is at least 180 days. However, depending on your employer, a full academic year can range from 170 days to 200 days. Whether you work full- or part-time, your service is based on the length of your school year:

For all BOCES and school district employees, as well as teachers working at New York State schools for the deaf and blind: Number of days worked ÷ 180 days

For college employees: Number of days worked ÷ 170 days

For institutional teachers: Number of days worked ÷ 200 days

Check Your Service Credit

You can sign in to Retirement Online and find your current estimated service credit listed on your Account Homepage under ‘My Account Summary.’

If you’re not sure whether you’re earning full-time or part-time service, you can check your most recent Member Annual Statement to see how much service you earned over the past fiscal year. To view your most recent Statement, sign in to Retirement Online. From your Account Homepage, click the “View My Member Annual Statement” button under ‘My Account Summary.’ If you are receiving full-time service, it will say “1.00 Years” for service credited from 4/1/2022 – 3/31/2023. A reminder: the total credited service you will see listed on your Statement was as of March 31, 2023.

If you’re planning to retire soon, it’s a good idea to take inventory of any debt you owe. Paying down your debt can give you flexibility to enjoy the type of retirement you want.

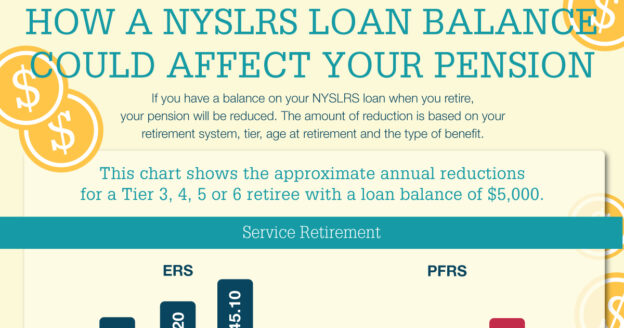

NYSLRS Loan Debt

If you have an outstanding NYSLRS loan balance when you retire, it will reduce your pension. The amount of your reduction is based on:

Your retirement system — Employees’ Retirement System (ERS) or Police and Fire Retirement System (PFRS);

Your tier;

Your age at retirement; and

Whether you retire with a service retirement benefit or a disability retirement benefit.

The pension reduction does not go toward repaying the outstanding loan balance — it’s a permanent reduction. And, at least part of the loan balance at retirement will be subject to federal income taxes.

When you apply to retire using Retirement Online and have an outstanding NYSLRS loan balance, the pension reduction amounts are provided to you. They are also listed on the loan applications on our Forms page. If you are nearing retirement, be sure to check your loan balance. If you are not on track to repay your loan before you retire, you can increase your loan payments, make additional lump sum payments or both (see the Change Your Payroll Deductions or Make Lump Sum Payments section of our Loans page.)

Although ERS members may repay their loan after retiring, they would have to pay the full balance that was due at retirement in a single lump sum payment. Then, going forward, the pension would be increased to the amount it would have been without the loan reduction. However, it would not be increased retroactively back to the date of retirement.

Other Debt to Check

Credit Cards

Another priority is paying off credit cards. Credit card statements carry a minimum payment warning that tells you how long it will take, and how much it will cost, to pay off your balance making only minimum payments.

If you have more than one credit card balance, many financial advisors recommend you pay as much as you can on the card with the highest interest, while making at least the minimum payments on lower-interest cards. Once you’ve paid off the high-interest card, focus on the one with the next-highest rate, and so on. Other advisors say it might be better to pay off the card with the smallest balance first. The idea is to gain a sense of accomplishment, and make the process seem less daunting.

Mortgages

Should you try to pay off your mortgage before you retire? Advice varies on that question. It would eliminate a major expenditure and let you spend your retirement income on other things. On the other hand, if your mortgage interest rate is relatively low, you may want to focus on paying off other high-interest debt or boosting your retirement savings. What works best for you will depend on your situation.

NYSLRS membership provides more than just retirement benefits. For most members, if you die while in active service, your beneficiary may be eligible to receive a death benefit. Here is an overview of member death benefits. If you are retired, visit our Death Benefit page for retirees to learn about your available benefits.

Types of Death Benefits

Most members who die while they’re still working will leave their beneficiaries what’s called an “ordinary death benefit.” This is a lump sum payment that’s usually equal to one year of your earnings per year of service, up to a maximum of three years.

Generally, to leave your beneficiaries this death benefit, you must have at least one year of service credit and your death must occur while you are on the public payroll.

Some members who die because of an on-the-job accident (not due to their own willful negligence) may leave their beneficiary an accidental death benefit. The accidental death benefit is a pension payable to your spouse. Other beneficiaries, as specified by law, may be eligible if there is no spouse.

For Employees’ Retirement System (ERS) Tier 4, 5 and 6 members, the benefit would be 50 percent of your earnings from your last year of service.

For most other members, the benefit would be 50 percent of your final average earnings (less any workers’ compensation benefit).

There is no minimum service credit requirement to leave an accidental death benefit.

The specific death benefits that may be available to your beneficiaries depend on your tier and retirement plan. Find Your NYSLRS Retirement Plan Publication and check it for specific benefit amount and eligibility information.

Note: For public employees who contract COVID-19 on the job and die from COVID-19, their beneficiaries may be eligible for an enhanced death benefit. Find out more about the Enhanced Death Benefit for Survivors of COVID-19 Victims.

Review and Update Your Beneficiaries

You should periodically review your beneficiary designations. Life circumstances sometimes change, and the beneficiary you may have named before might not be the one you would choose today. You should also make sure your beneficiary’s contact information is up to date so we can find them when needed.

Retirement Online is the best way to manage your beneficiary information. Sign in to Retirement Online today and click “View and Update My Beneficiaries” to review your named beneficiaries, and update them if needed.

Reporting a Death

NYSLRS cannot pay out death benefits until after we are notified of a member’s death and have a certified copy of the death certificate. The fastest way for survivors to report a member’s death to NYSLRS is using our online form on our website. Survivors can also upload a copy of the certified death certificate, which enables us to start reaching out to the beneficiary. It’s important to talk with your family about your benefits and how to report your death to NYSLRS.

Payment of Death Benefits

NYSLRS will reach out to your beneficiaries on file and send them the application and instructions for receiving benefits. NYSLRS can pay death benefits once it receives the required documentation.

The celebration of everything New York begins Wednesday, August 23 and runs through Monday, September 4 (Labor Day). Our information representatives will be at the fairgrounds in Syracuse from 10:00 am to 9:00 pm to help members and retirees with their retirement planning and benefit questions. You’ll also be able to pick up retirement plan brochures and forms, request an estimate that will be mailed to you and get help registering for a Retirement Online account.

The NYSLRS booth will be in the Center of Progress Building, Building 3 on the State Fair map, near the Main Gate.

Find Unclaimed Funds at the State Fair

OSC’s Office of Unclaimed Funds booth will also be in the Center of Progress Building. An unclaimed fund is lost or forgotten money, perhaps in an old bank account or insurance policy, that has been turned over to the State. See if any of that money is yours. So far this year, State Comptroller Thomas P. DiNapoli and the Office of Unclaimed Funds have returned more than $295 million.

Special Fair Days

Wednesday, August 23

Opening Day — Governor’s Day

Thursday, August 24

Student Youth Day — Youth and students under 18 years of age are admitted free on this day. ID showing date of birth may be requested.

Agriculture Career Day

Friday, August 25

Pride Day — The first State fair in America to host an official Pride Day to celebrate the LGBTQIA+ community.

New Americans Day

Monday, August 28

Law Enforcement Day — Free admission to any active or retired law enforcement or corrections personnel who present a badge or picture ID from the department from which they are or were employed.

Tuesday, August 29

Comptroller DiNapoli Visits the Fair — He is the trustee of the New York State Common Retirement Fund and is the administrator of NYSLRS. He will present area residents and organizations with unclaimed funds, and he’ll be stopping by the NYSLRS booth during the day.

Fire & Rescue Day — Free admission to any active or retired member of a fire department or emergency services organization who presents a picture ID from that department or organization.

Beef Day

Wednesday, August 30

Women’s Day

Thursday, August 31

Armed Forces Day — Free admission to any active-duty service member or veteran with military identification (military ID card, form DD-214 or NYS driver license, learner permit or nondriver ID card with a veteran designation).

Dairy Day

Stomp Out Stigma Day

Friday, September 1

Native American Day — Free admission to all members of Native American tribes, no ID required.

Looking for some summer reading to add to your e-reader? Check out these publications from NYSLRS for important retirement information.

1. Retirement Plan for ERS Tier 6 Members (Article 15)

Are you one of more than 350,000 Tier 6 Employees’ Retirement System (ERS) members covered by Article 15? Your retirement plan publication explains some of the benefits and the services available to you, including service retirement, disability retirement, death benefits and more. Read it now.

2. Retirement Plan for ERS Tier 3 and 4 Members (Articles 14 and 15)

If you’re not in Tier 6, you’re likely among more than 260,000 Tier 3 and 4 ERS members covered by Article 14 and 15. Check out your publication to find out about the benefits and the services available to you. Read it now.

3. Service Credit for Tiers 2 Through 6

The service credit you earn as a NYSLRS member is an important factor in the calculation of your pension. This publication explains the service you can earn credit for and how you can request to purchase credit for additional public employment or military service. Read it now.

4. What If I Leave Public Employment?

While we hope you stay a NYSLRS member throughout your working career, we understand that circumstances can change. If you leave public employment, this publication explains what you’ll need to do and what happens to your NYSLRS membership. Spoiler: It depends on how much service you have. Read it now.

5. What If I Work After Retirement?

Generally, NYSLRS retirees under age 65 can earn up to $35,000 per calendar year from public employers in New York State without affecting their NYSLRS pension. However, you should be aware of the laws governing post-retirement employment and how working after retirement may impact your retirement benefits. If you are considering working while collecting your pension, you should read this publication. If you already work in public employment as a NYSLRS retiree, read our Update Regarding Retiree Earnings Limit blog post for information about recent legislation and Governor’s executive orders that affect the limit.

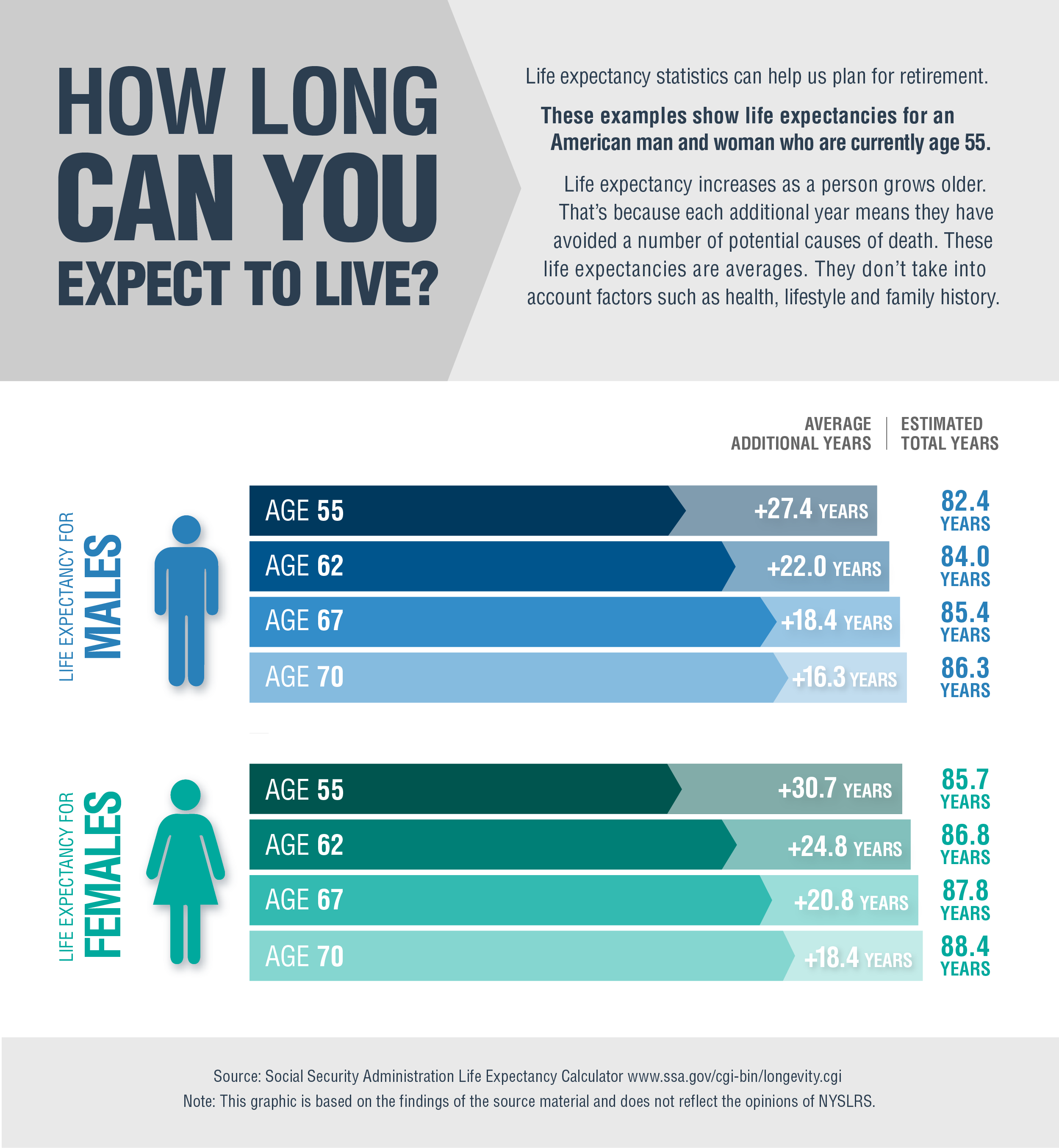

As you plan for retirement, you need to think about your sources of income in retirement. However, you should also consider how long your retirement income will need to last.

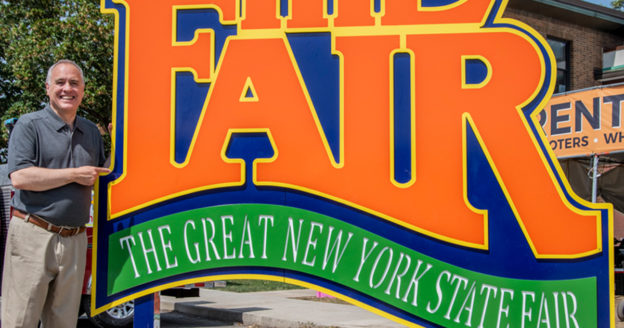

Longer Life Span, Longer Retirement

These days, a 55-year-old man can expect to live for another 27.4 years, to about 82. A 55-year-old woman can expect to live for more than 30 years. These figures, derived from the Social Security life expectancy calculator, are only averages. They don’t account for factors such as health, lifestyle or family medical history.

Here are some other statistics worth considering as you plan for retirement (as of the State fiscal year that ended March 31, 2022):

More than 37,000 NYSLRS retirees were over 85 years old;

More than 3,500 had passed the 95-year mark; and

401 NYSLRS’ retirees were 101 or older.

Considering that many public employees can retire as early as 55, it’s possible that a fair number of them could have retirements that last 45 years or more.

Saving for a Long Retirement

Your NYSLRS pension is one source of income that you can depend on however long your retirement lasts. Employees’ Retirement System (ERS) members who retired in fiscal year 2022 are receiving an average monthly pension of $2,748. Social Security is another long-term source. The average Social Security benefit for a retired worker was $1,837 a month, as of June 2023.

Your retirement savings is a crucial asset that can supplement your pension and Social Security. In a long retirement, savings can help with rising costs and provide a source of cash in an emergency.

It is never too late to start saving for retirement. The New York State Deferred Compensation Plan is one easy way to get started. It’s a program created for New York State employees and employees of participating public agencies. If you’re a municipal employee, ask your employer if you’re eligible for the Deferred Compensation Plan or another retirement savings plan. (The New York State Deferred Compensation Plan is not affiliated with NYSLRS.)

You should also visit our Start Saving for Retirement page. You’ll find an example of how much you can save over a 30-year period, and a sample withdrawal strategy designed to provide retirement income for 20 years.

New York Retirement News is dedicated to keeping NYSLRS members and retirees informed about developments that may affect their benefits. In case you missed them, or just want to take another look, here are some of our most popular blog posts from the past year.

Becoming Vested Becoming vested is a crucial milestone in your NYSLRS membership. Under legislation enacted in April 2022, Tier 5 and 6 members are now vested after five years of service. Previously, these members needed ten years of service credit to be eligible for a service retirement benefit.

Update Regarding Retiree Earnings Limit Normally, most NYSLRS retirees who return to work for a public employer are limited in how much they can earn before their pension would be suspended. The limit is $35,000 per calendar year, however, executive orders from the Governor and legislation temporarily suspended this limit. Read the blog post for current information.

Enhanced Death Benefit for Survivors of COVID-19 Victims Survivors of NYSLRS members who contract COVID-19 on the job may be entitled to an enhanced death benefit if the member dies as a result of the disease. This accidental death benefit covers eligible deaths through December 31, 2024.

Find Your Retirement Plan Publication Your retirement plan publication is an essential resource that provides comprehensive information about your NYSLRS benefits. It explains how long you’ll need to work to receive a pension, how your benefit is determined, what death and disability benefits may be available and more. Our new tool can help you find your plan publication.

What is a Defined Benefit Plan? As a NYSLRS member, you are part of a defined benefit plan, also known as a traditional pension plan. Defined benefit plans are often confused with defined contribution plans, but there are major differences between the two types of plans.

While most New York teachers and administrators are in the

While most New York teachers and administrators are in the