Most NYSLRS members contribute a percentage of their earnings to the Retirement System. Over time, those contributions, with interest, can add up to a tidy sum. But what happens to that money? Will you get your contributions back when you retire? The answer to that question is “no.” Let’s look at what happens to your NYSLRS contributions.

How NYSLRS Retirement Plans Work

NYSLRS plans are defined benefit pension plans. Once you’re vested, you’re entitled to a lifetime benefit that will be based on your years of service and final average earnings. The amount of your contributions does not determine the amount of your pension. (Use Retirement Online to estimate your pension.)

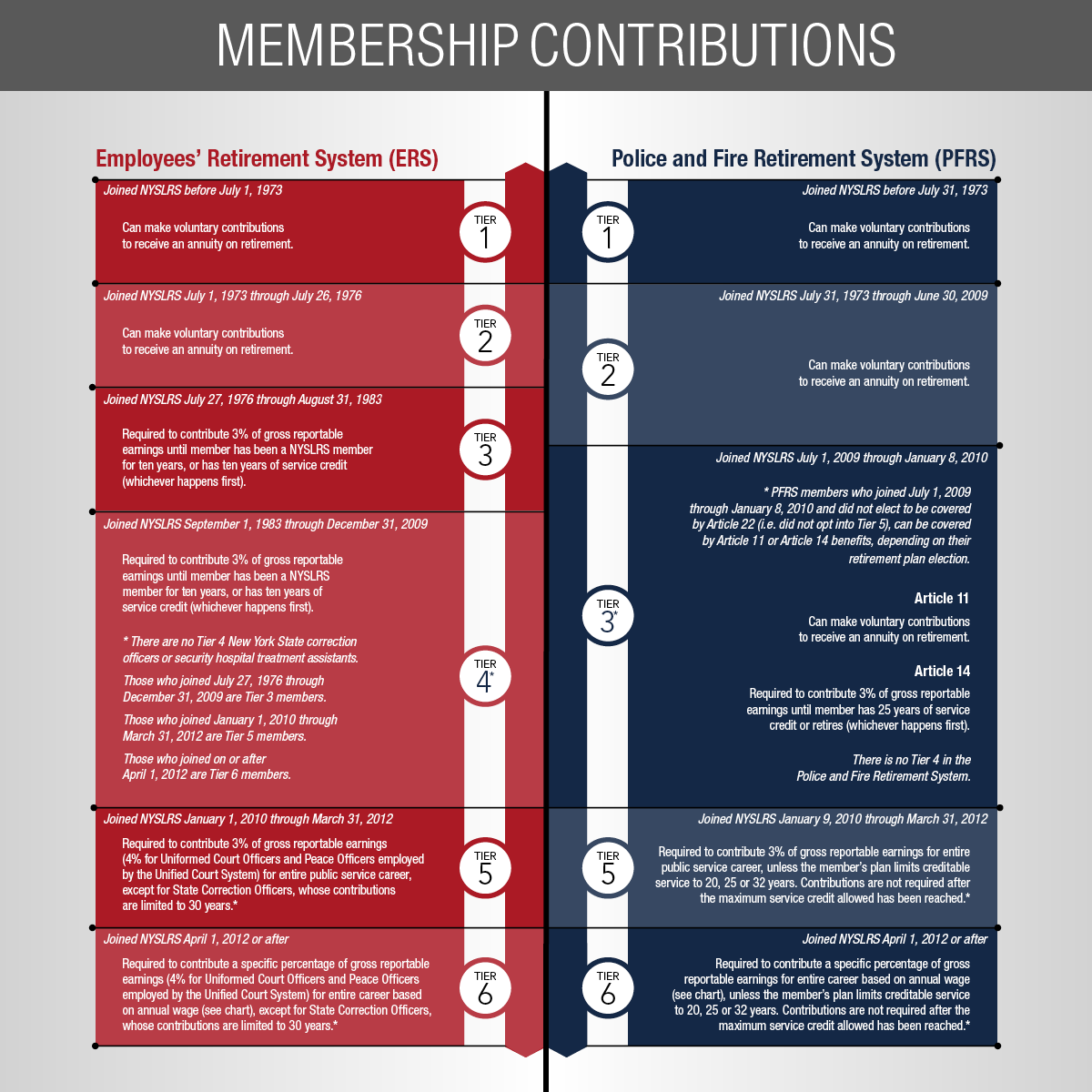

Your NYSLRS plan differs from defined contribution plans, such as a 401-k plan, which are essentially retirement savings plans. In those plans, a worker, their employer, or both contribute to an individual retirement account. The money is invested and hopefully accumulates investment returns over time. This type of plan does not provide a guaranteed lifetime benefit and there is the risk that the money will run out during the worker’s retirement years. Experts recommend that workers who have defined contribution plans contribute anywhere from 10 to 20 percent of their income to their plan. NYSLRS members, in contrast, contribute between 3 and 6 percent of their income, depending on their tier and retirement plan.

Where Your Contributions Go

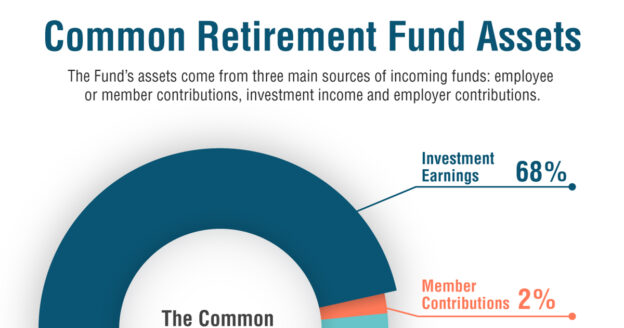

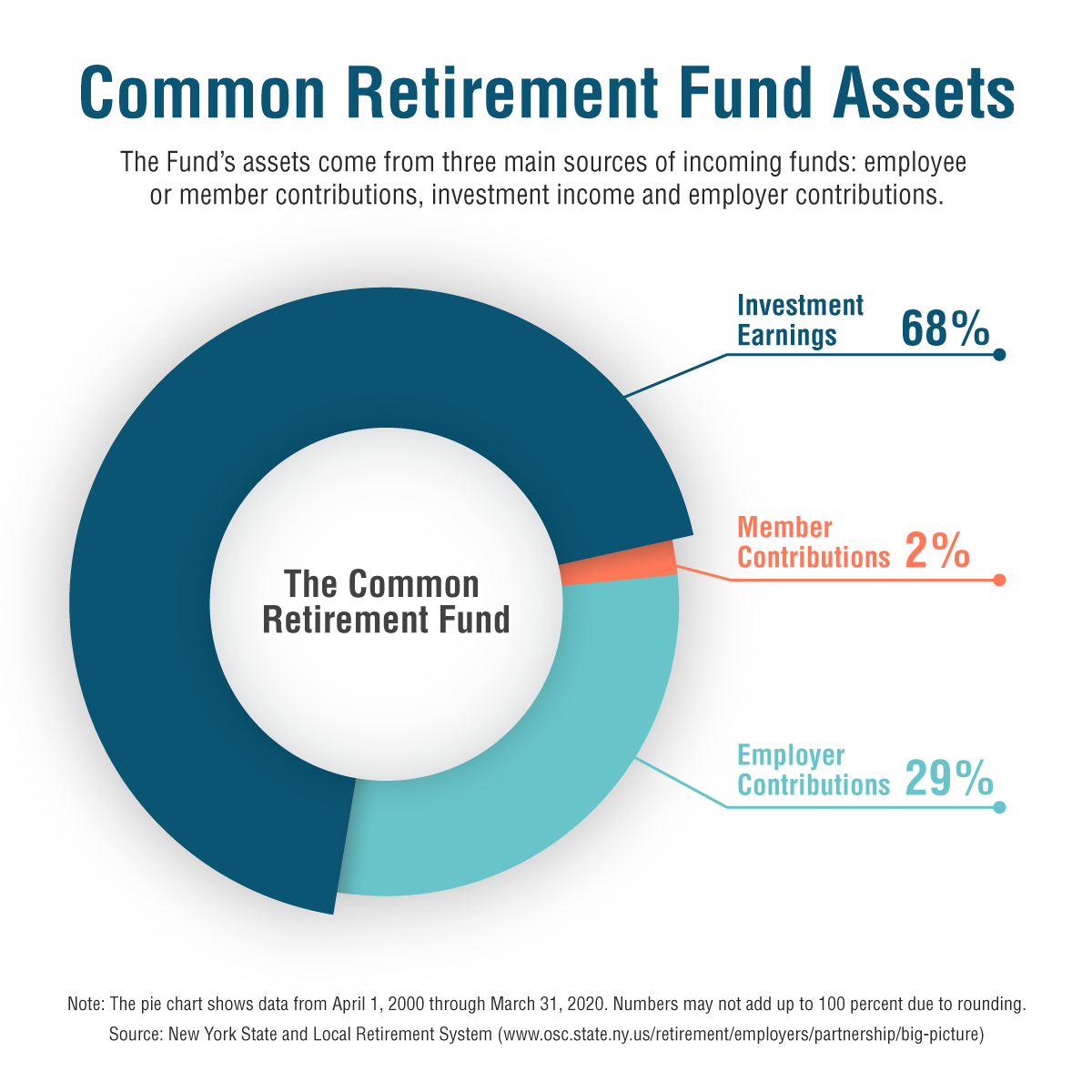

When you retire, your contributions go into the New York State Common Retirement Fund. The Fund is the pool of money that is invested and used to pay retirement benefits for you and other NYSLRS members.

Your Contribution Balance

You can find your current contribution balance in Retirement Online. But if your contributions don’t determine your pension, what difference does it make what the balance is? For one thing, your contribution balance helps determine the amount you can borrow if you decide to take a loan from NYSLRS. Also, you may be able to withdraw your contributions, with interest, if you leave the public workforce before retirement age.

Withdrawing Your Contributions

You cannot withdraw your contributions while you are still working for a public employer in New York State. If you leave public employment with less than ten years of service, you can withdraw your contributions, plus interest. If you withdraw, you will not be eligible for a NYSLRS retirement benefit.

If you have more than ten years of service, you cannot withdraw, but you will be entitled to a pension when you reach retirement age. But remember, you will not receive this pension automatically; you must file a retirement application before you can receive any benefit.

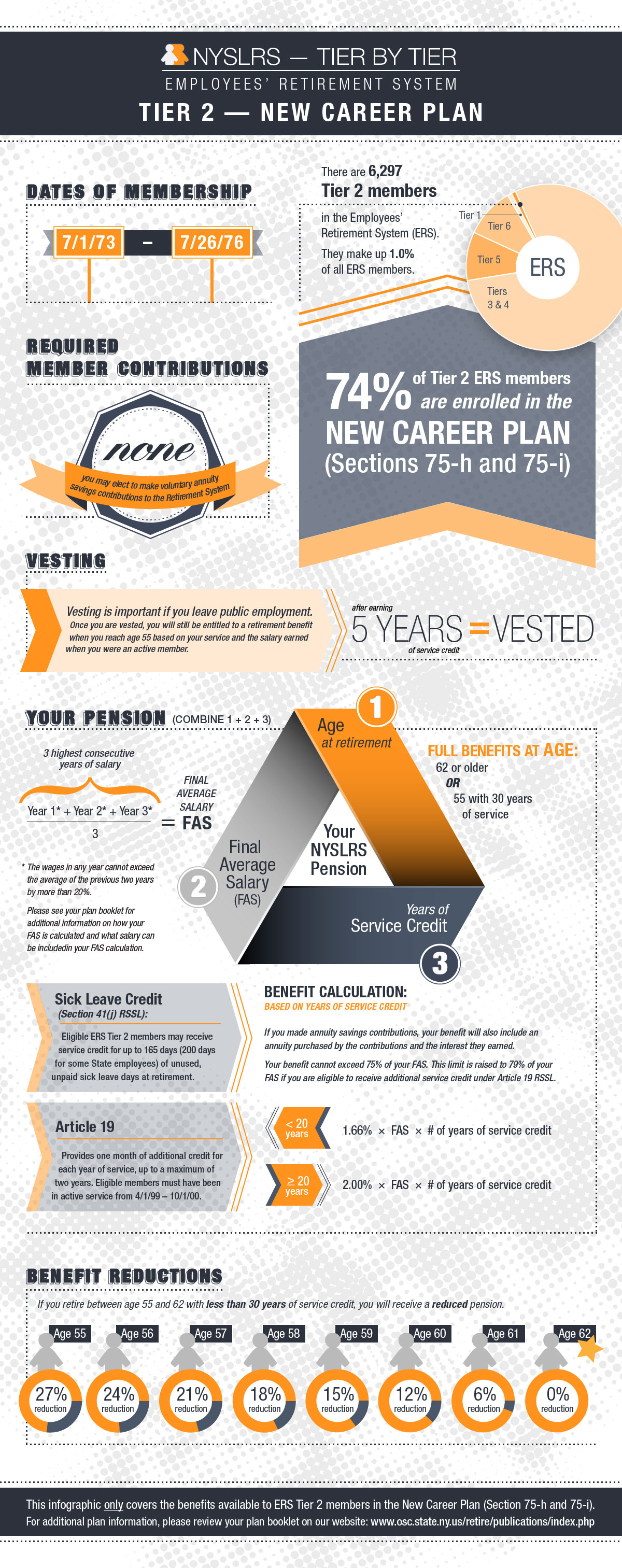

If you’re an ERS Tier 2 member in an alternate plan, you can find your retirement plan publication below for more detailed information about your benefits:

If you’re an ERS Tier 2 member in an alternate plan, you can find your retirement plan publication below for more detailed information about your benefits: